Industry Updates

Updated 4/22/24: Summary of the 2024 Housing Laws

Published 4/22/2024 at 4:43 PM

By: Rosenberg & Estis, P.C.

On April 20, 2024 as part of the Budget Legislation, NYS Governor Hochul signed into law major new and amended housing laws which will reshape residential development and ownership in New York City and New York State. Rosenberg & Estis, P.C. has been closely tracking the new housing laws and will be presenting webinars about them starting the week of April 29, 2024. Please watch for an invitation to our first webinar on these new laws. Below is our initial summary of some of the major changes we will discuss in more detail at our upcoming webinars, which should not be construed as client advice.

I. 421-a(16) Completion Date Extension – Must Be Requested Within 90 Days of HPD Issuing Form of “Letter of Intent”

II. Affordable Neighborhoods for New Yorkers Tax Incentive or “ANNY” – RPTL 485-x

III. Affordable Housing from Commercial Conversions Tax Incentive Benefits or “AHCC” – RPTL 467-m

IV. Good Cause Eviction – Amendments of Real Property Law and Real Property Actions and Proceedings

V. Individual Apartment Increases (“IAIs”) – Amendment of the Emergency Tenant Protection Act and Rent Stabilization Law

VI. Lifting 12.0 Residential Floor Area Ratio Cap of Certain Dwellings

Here’s a quick summary of some of the major changes we will be discussing:

I. 421-a(16) Completion Date Extension – Must Be Requested Within 90 Days of HPD Issuing Form of “Letter of Intent”

Part T of the Budget Legislation amends the 421-a(16) program to allow certain projects an additional 5 years, until June 15, 2031, to achieve their Completion Date. Projects which have vested for 421-a(16) through a Commencement Date on or before June 15, 2022 are currently required to achieve a Completion Date (TCO of CO for all residential areas) on or before June 15, 2026. NYS has amended 421-a(16)’s definition of “Eligible Multiple Dwelling” to allow for this extension provided such project does not use Affordability Option “C” or “G” (both of which allow project to provide 30% of units affordable at or below 130% of Area Median Income “AMI”). Projects must file a “Letter of Intent” with HPD requesting the extension within 90 days of HPD issuance of a Letter of Intent Form (HPD issuance required by June 19, 2024) to qualify for this Completion Date extension. If you are interested in a Completion Date extension for your 421-a(16) project, please contact your trusted R&E attorney or Daniel M. Bernstein.

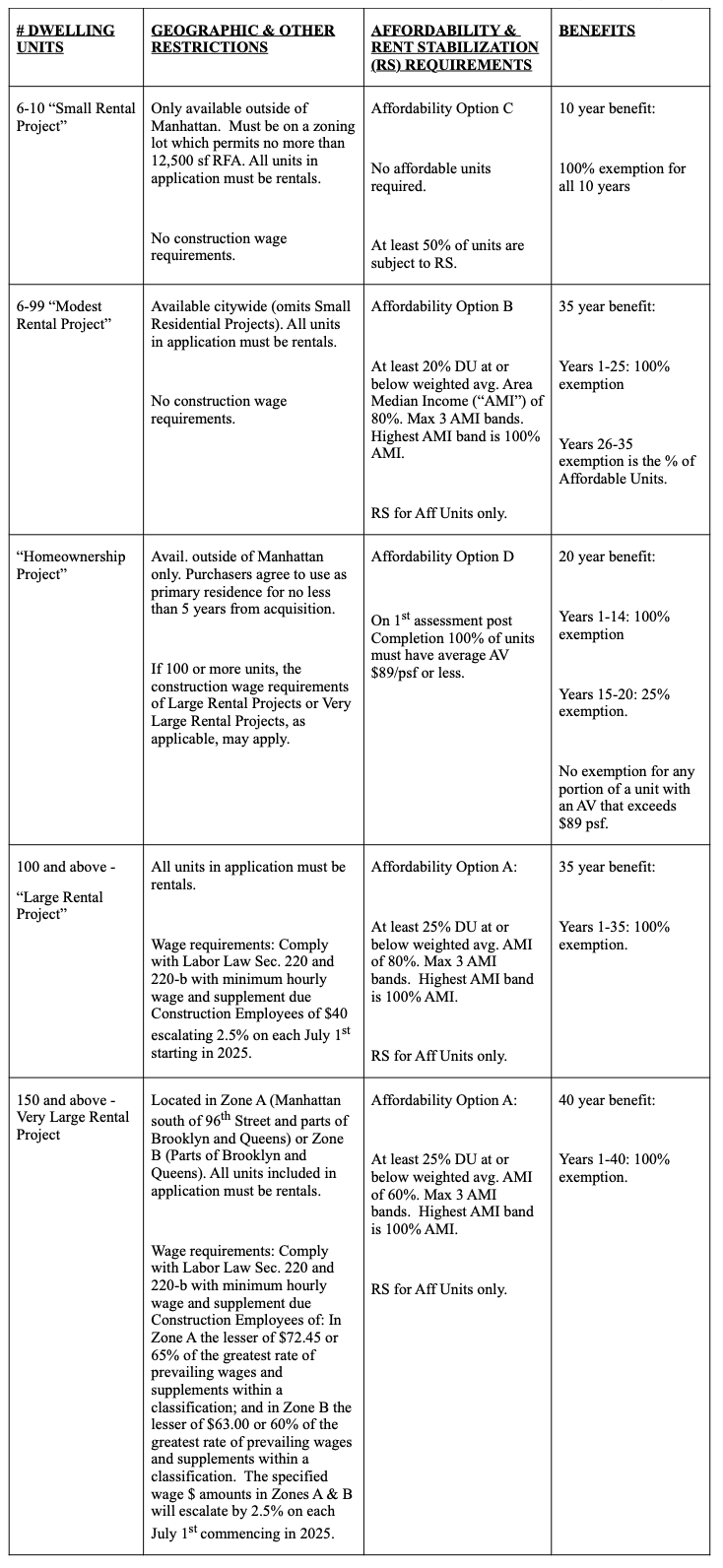

II. Affordable Neighborhoods for New Yorkers Tax Incentive or “ANNY” – RPTL 485-x

Part U of the Budget Legislation creates the ANNY program which provides a 10, 20, 35 or 40 year property tax exemption for eligible new construction projects and is a replacement of the expired 421-a program. Residential new multiple dwellings and eligible conversions can qualify for ANNY if they have a Commencement Date on or after June 16, 2022 and on or before June 15, 2034 and must have a Completion Date on or before June 15, 2038.

ANNY program similarities to the expired 421-a(16) program:

- Exemption is of the percentage of increase in assessed value (“AV”) above the AV from the tax year prior to Commencement Date (the “Prior AV”).

- Prevailing wage requirement for building service employees during the ANNY program benefit period.

- ANNY program benefits are reduced if the floor area of a project’s eligible commercial, community facility, and accessory use space exceeds 12% of the project’s aggregate floor area.

- The unit mix of affordable housing units must pass either the “proportionality” or “two-bedroom” test.

- All Restricted Units (Affordable Housing Units and RS Units in a Small Rental Project) must share the same common entrances and common areas as market units and shall not be isolated to a specific floor or area of building.

- Replacement Ratio applies if an Eligible Site contained dwelling units within 3 years prior to the Commencement Date which dwelling units were demolished, removed or reconfigured.

Notable differences between the ANNY program and the expired 421-a(16) program:

- The ANNY program restriction period extends in perpetuity; affordable housing units are permanently subject to the affordability requirement and rent stabilization. rent stabilized units are permanently subject to rent stabilization.

- Market units (units other than Restricted Units) are not subject to rent stabilization (unless otherwise subject in the absence of ANNY program benefits) – no requirement to meet or exceed the high-rent threshold for exemption from rent stabilization.

- The ANNY program includes explicit violations/penalties for the failure to comply with the construction wage, prevailing wage, affordability and rent stabilization requirements.

- Construction Wage requirements apply to Large Rental Projects (100 units and above) and Very Large Rental Projects (150 units and above in designated locations). Homeownership Projects which meet these unit counts would also be subject to Construction Wage requirements.

- Very Large Projects can receive up to 5 years of construction benefits and during the construction period or extended construction period do not pay taxes even on the prior assessed value (i.e. no mini-tax).

- Homeownership projects must have an initial post-completion average assessed value at or below $89 psf.

- Minority and Women Owned Business Enterprises (“MWBEs”): An Eligible Site must make all reasonable efforts to spent on contracts with MWBEs at least 25% of the total applicable costs as MWBEs and applicable costs are defined in rules of HPD.

- Application filing fee varies according to size of project: $3,000 per dwelling unit for Eligible Sites with 6-10 units; $4,000 per dwelling unit for Eligible Sites with 12-99 units; $5,000 per dwelling unit for homeownership projects; and $5,000 per dwelling unit for Eligible Sites with 100 or more units. HPD can promulgate rules for lesser fees for Eligible Sites containing Eligible Multiple Dwellings constructed with the substantial governmental assistance of grants, loans or subsidies provided by a federal, state or local governmental agency or instrumentality pursuant to a program for the development of affordable housing. Due to a drafting error, it appears that ANNY projects with 11 units have no Application filing fee listed.

If you are interested in qualifying a residential project for benefits under ANNY / 485-x, please contact your trusted R&E attorney or Daniel M. Bernstein or Nicholas DiLorenzo.

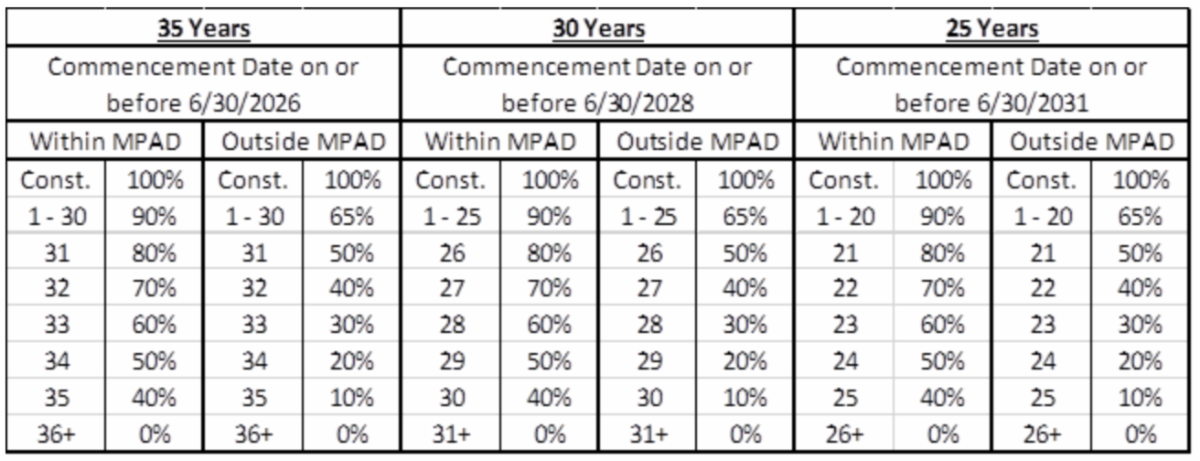

III. Affordable Housing from Commercial Conversions Tax Incentive Benefits or “AHCC” – RPTL 467-m

Part R of the Budget Legislation creates the AHCC program which provides a 25, 30, or 35 year property tax exemption for non-residential buildings converted to eligible multiple dwellings that meet certain construction and affordability criteria. Eligible conversions can qualify for AHCC program benefits if they have a commencement date on or before June 30, 2031, and a completion Date on or before December 31, 2039.

Non-residential building means a structure or portion of a structure, except a hotel or other class B multiple dwelling, having at least one floor, a roof and at least three walls enclosing all or most of the space used in connection with the structure or portion of the structure, which has a certificate of occupancy for commercial, manufacturing or other non-residential use for not less than 90% of the aggregate floor area of such structure or portion of such structure, other proof of such non-residential use as is acceptable HPD.

Eligible Multiple Dwellings under the AHCC program must contain at least six residential rental units and must meet the “affordability requirement” whereunder:

- not less than 25% of the dwelling units are affordable housing units;

- not less than 5% of the dwelling units are affordable to and restricted to occupancy by individuals or families whose household income does not exceed 40% of AMI;

- the weighted average of all income bands for all of the affordable housing units does not exceed 80% of AMI;

- there are no more than three income bands; and

- no income band exceeds 100% of AMI.

Part R of the Budget Legislation also includes RPTL 467-m within the meaning of “paid for in whole or in part out of public funds” under Section 224-a of the Labor Law, which could impose a prevailing wage requirement for construction workers in connection with AHCC program benefits. This aspect of the Budget Legislation requires further analysis and/or clarification from the Legislature.

AHCC program benefits are increased for projects located in the Manhattan prime development area (i.e., in Manhattan entirely south of 96th Street; “MPAD”), and projects with an earlier commencement date have a longer benefit duration:

AHCC program similarities to the expired 421-a(16) program:

- Prevailing wage requirement for building service employees during the AHCC program benefit period.

- AHCC program benefits are reduced if the floor area of a project’s eligible commercial, community facility, and accessory use space exceeds 12% of the project’s aggregate floor area.

- The unit mix of affordable housing units must pass either the “proportionality” or “two-bedroom” test.

- All affordable housing units must share the same common entrances and common areas as market units and shall not be isolated to a specific floor or area of building.

- Application filing fee of $3,000 per dwelling unit.

Notable differences between the AHCC program and the expired 421-a(16) program:

- No “mini tax”; the exemption percentage is applied to the real property taxes due in the applicable exemption year (other than local assessments) but subject to the reduction discussed above.

- The AHCC program restriction period extends in perpetuity; affordable housing units are permanently subject to the affordability requirement and rent stabilization.

- Market units are not subject to rent stabilization (unless otherwise subject in the absence of AHCC program benefits) – no requirement to meet or exceed the high-rent threshold for exemption from rent stabilization.

- The AHCC program includes explicit violations/penalties for the failure to comply with the prevailing wage and affordability requirements.

If you are interested in qualifying a non-residential conversion project for benefits under AHCC / 467-m, please contact your trusted R&E attorney or Daniel M. Bernstein or Nicholas DiLorenzo.

IV. Good Cause Eviction – Amendments of Real Property Law and Real Property Actions and Proceedings

Part HH of the NYS Budget Legislation includes the widely discussed Good Cause Eviction (“GCE”), applicable to residential apartments in the City of New York and available to other municipalities that choose to opt-in. The substantive provisions are contained in a new Article 6A of the Real Property Law (“RPL”), with corresponding amendments to a number of provisions of the Real Property Actions and Proceedings Law (“RPAPL”). Generally, GCE prevents landlords from evicting a tenant other than for the good cause reasons enumerated in the statute, which includes eviction for non-payment where a rent increase is not unreasonable. An increase that does not exceed the lesser of 10% or 5% plus the annual Consumer Price Index percentage increase (“local rent standard”) is presumptively reasonable. The following is a summary of the salient provisions.

All “Housing Accommodations” are subject to the provisions of GCE, unless they satisfy one of the enumerated exemptions. Housing Accommodations are defined as any “residential premises,” regardless of the number of units and including mixed use residential premises. Based on the provisions of the law, it appears that residential premises refers to buildings as opposed to individual units.

The exemptions from GCE are as follows:

- Housing accommodations owned by “small landlords”, defined as owners of fewer than 10 units in the State. Note, however, that beneficial interests in entities owning more than 10 units in the State will defeat the exemption, and the burden is on the owner entity to disclose all natural persons with beneficial interests in order to obtain an exemption;

- Owner occupied housing accommodations with fewer than ten units;

- Units which are sublet, where the sublessor seeks to recover the unit for their own use;

- Units occupied solely incident to employment, where such employment was, or will be, lawfully terminated;

- Units otherwise subject to regulation of rents or evictions under local, state or federal law;

- Units subject to affordability requirements pursuant to statute, regulation, restrictive declaration or regulatory agreement;

- Units within a housing accommodation owned as a cooperative or condominium, or in a housing accommodation that is subject to an offering plan submitted to the Attorney General;

- Housing accommodations for which a temporary or permanent certificate of occupancy was issued on or after January 1, 2009 for a period of thirty years following issuance of such certificate;

- Housing accommodations that qualify as seasonal use dwelling units;

- Housing accommodations located in a hospital, continuing care retirement community, assisted living facility, adult care facility, senior residential community and not-for-profit independent retirement communities;

- Manufactured homes on or in a manufactured home park;

- Hotel rooms or other transient use covered by the definition of a class B multiple dwelling;

- School dormitories;

- Housing accommodations within or for the use of a religious facility or institution; and

- Units within a housing accommodation in a municipality, other than the City of New York, for which the rent exceeds 245% of the monthly fair market rent published by HUD for the county in which the housing accommodation is located.

No landlord may evict a tenant from a housing accommodation covered by the statute, except for good cause and regardless of whether the tenant has no written lease or the term of the written lease has expired or otherwise terminated. Good cause is defined to including the following:

- Failure to pay rent due and owing, provided that the failure to pay rent did not result from an unreasonable rent increase. A rent increase is reasonable if it does not exceed the “local rent standard.” In addition, if the rent increase exceeds the “local rent standard”, there is a rebuttable presumption that it is unreasonable. The Court may consider all relevant facts to determine if the rent increase is reasonable, including, but not limited to, fuel and other utility costs, insurance, maintenance, increases in property tax expenses and significant repairs. Significant repairs include structural repairs, electrical, plumbing or mechanical repairs requiring a permit, abatement of hazardous materials, such as lead paint, asbestos or mold and exclude cosmetic repairs such as painting and decorating;

- Breach of a substantial obligation of tenancy, after ten-day written notice and an opportunity to cure;

- Conduct constituting a nuisance or which interferes with the comfort or safety of landlord or other tenants or occupants of the building or an adjacent building, or is maliciously or by gross negligence damaging the unit, the building in which it is located or the real property;

- Occupancy which constitutes or causes a violation of law which subjects the landlord to civil or criminal penalties and an agency of the municipality or State issues of vacate order, provided that the Court finds that (i) the violation cannot be cured unless the tenant vacates and (ii) the landlord did not create the condition necessitating the vacate order by neglect, intentional act or failure to act;

- Use of the housing accommodation for illegal purposes;

- Failure to provide access for necessary repairs or improvements required by law or to show the housing accommodation to prospective purchasers, mortgagees or others having a legitimate interest therein;

- Recovery for landlord’s personal use as its principal residence or for the use of landlord’s family members as defined in the statute. The standard for landlord’s recovery is a good faith intention to recover possession by clear and convincing evidence. This provision does not apply to housing accommodations occupied by a tenant who is sixty-five or older or is a disabled person;

- Recovery of the housing accommodation where the landlord has a good faith intention to demolish it.

- Recovery of the housing accommodation where the landlord has a good faith intention to withdraw it from the rental market.

- Tenant’s refusal to agree to reasonable changes to a renewal ease, including, but not limited to, a reasonable rent increase, provided that the proposed changes were provided no more than 90 and no less than 30 days prior to the expiration of the lease term.

In addition to creating a new Article 6-A of the RPL, the statute also creates RPL 231-c, which requires a landlord to append to any lease or renewal lease a notice disclosing whether or not the GCE law applies to the lease. The RPL 231-c notice must advise the tenant as follows:

- Whether the unit is exempt from GCE and, if so, the basis for the exemption;

- If the unit is subject to GCE, and the landlord intends to increase the rent above the local rent standard, the justification for the increase;

- If the unit is subject to GCE and landlord is electing not to renew the lease, the basis for such non-renewal.

Finally, the statute amends the notice requirements under RPL 226-c (Rent Increase or Non-Renewal) and RPAPL 711(2) (Rent Demand) by requiring that such notices include the RPL 231-c disclosures set forth above. Similarly, RPAPL 741 (Contents of Petition) is amended to require that the RPL 231-c disclosures must be appended to or incorporated into any Petition filed in a summary proceeding.

Article 6-A of the RPL is effective immediately and shall apply to all actions or proceedings commenced on or after the effective date. The remaining provisions are effective 120 days after they become law.

All of the foregoing provisions sunset on June 15, 2034.

If you are interested in discussing Good Cause Eviction’s impact on your properties, please contact your trusted R&E attorney or Deborah E. Riegel.

V. Individual Apartment Increases (“IAIs”) – Amendment of the Emergency Tenant Protection Act and Rent Stabilization Law

Part FF of the Budget Legislation amends the Emergency Tenant Protection Act (ETPA) and Rent Stabilization Law (RSL) with respect to aggregate costs and caps of individual apartment improvement (IAI) increases for rent stabilized apartments. The amendment provides for two tiers of IAI increases and takes effect in 6 months.

Tier One:

- Increases the cap on aggregate cost of IAIs to $30,000 performed in a 15 year period, beginning with the first IAI after June 14, 2019. Places no limit on the number of separate IAIs in the 15 year period.

- The Tier One IAI increase is permanent and available for vacant apartments as well as for occupied apartments with written consent in the tenant’s primary language.

- Maintains the HSTPA’s IAI increase of 1/180th of the IAI cost for buildings with more than 35 apartments and 1/168th of the IAI cost for buildings with 35 or fewer apartments. Accordingly:

- For a building with more than 35 apartments, the maximum Tier One IAI increase is $166.67 (1/180th of $30,000).

- For a building with 35 or fewer apartments, the maximum Tier One IAI increase is $178.57 (1/168th of $30,000).

Tier Two:

- Increases the cap on aggregate cost of IAIs to $50,000 performed in a 15 year period, beginning with the first IAI after June 14, 2019.

- The Tier Two IAI increase is permanent and is only available for vacant apartments.

- Eligibility for the Tier Two increase requires that either one of the following two criteria be satisfied, along with receipt of prior certification from DHCR (“the Tier Two Eligibility Criteria”),:

- The apartment must have been timely registered as “vacant” by no later than December 31st in each of 2022, 2023 and 2024. A landlord may recover costs no more than once under this criterion.

- The apartment is vacant following a period of continuous occupancy of at least 25 years that occurred immediately prior to the commencement of the IAI. There is no limit on the number of separate IAIs in the 15 year period under this criterion.

-OR-

- The IAI increase is increased to 1/156th of the IAI cost for buildings with more than 35 apartments and 1/144th of the IAI cost for buildings with 35 or fewer apartments. Accordingly:

- For a building with more than 35 apartments, the maximum Tier Two IAI increase is $320.51 (1/156th of $50,000).

- For a building with 35 or fewer apartments, the maximum Tier Two IAI increase is $347.22 (1/144th of $50,000)

- Immediately subsequent to undertaking the IAI, the landlord must submit to DHCR any evidence of the work that DHCR deems necessary and must pay a fee equaling 1% of the amount claimed for the IAI.

- An owner will be in eligible for the Tier Two IAI increase if, within the 5 year period prior to filing, any unit within any building owned by any partial or beneficial owner of the building in which the IAI unit is located has been subject to a treble damages award or harassment determination.

If you are interested in discussing the new IAI law’s impact on your properties, please contact your trusted R&E attorney or Zachary Rothken.

VI. Lifting 12.0 Residential Floor Area Ratio Cap of Certain Dwellings.

Part Q of the Budget Legislation amends the State Multiple Dwelling Law to allow localities to increase the maximum allowable residential floor area ratio (FAR) above the decades-long 12 FAR “cap.” However, it does so with certain caveats and conditions.

In NYC developments or enlargements having a residential FAR greater than 12 may not be located:

- in a historic district; or

- on a zoning lot containing joint living-work quarters for artists or residential lofts subject to the Loft Law.

In addition, new developments having a residential FAR greater than 12 may not be located on a zoning lot containing an existing multiple dwelling having an FAR less than 12, unless such existing multiple dwelling has been issued a certificate of no harassment (CONH). Where such existing multiple dwellings are to be demolished, in addition to obtaining a CONH, the owner must provide each tenant in residency for a minimum of six months either:

- a payment equal to one month’s rent for each year of residency, or

- a lease at a “comparable rent in a decent, safe, and sanitary dwelling in an area not less generally desirable.”

Finally, new developments having a residential FAR greater than 12, must provide permanent affordable housing “equivalent to or exceeding” the applicable requirements of the City’s Mandatory Inclusionary Housing (MIH) program.

The same requirements apply to general project plans adopted by the NYS Urban Development Corporation (UDC), except that:

-

- instead of providing affordable housing in compliance with the City’s MIH program, a minimum 25% of the dwelling units must be affordable to households having an average 80% of area median income; and

- such general project plans must include a “feasible method” for relocating any displaced families to “decent, safe, and sanitary dwellings” either in the project area or another area “not generally less desirable,” “reasonably accessible to their places of employment,” and at rents “within the [families’] financial means.”

In anticipation of the FAR cap being lifted, the Department of City Planning’s City of Yes for Housing Opportunity (COYHO) zoning text amendments propose the creation of two new high-density zoning districts, R11 and R12, which would allow, respectively, 15 and 18 FAR with the provision of affordable housing. The COYHO text amendments are currently in public review with final approval anticipated by the end of 2024.

If you are interested in discussing the FAR cap change’s impact on your properties, please contact your trusted R&E attorney or David J. Rosenberg.