NYC Property Tax

NYC Pied-à-Terre Surcharge is Law: 3 Months to Prepare for the 1st Non-Primary Residence Notice

Published 6/1/2026 at 1:07 PM

By: Benjamin M. Williams

Governor Kathy Hochul signed A10009C into law on May 28, 2026. Part HH of the budget bill creates a new annual New York City surcharge on certain high value residential properties that do not serve as a primary residence.

This is commonly being called the pied-à-terre tax. Technically, the law calls it a surcharge on property that does not serve as a primary residence. It is not a transfer tax imposed when a property is sold. It is an annual charge that will be imposed in addition to ordinary New York City real property taxes.

The surcharge applies beginning with the New York City tax year that starts on July 1, 2026, and the law expires after five years on June 30, 2031, unless extended. For the first year, the first payment is due January 1, 2027.

The most important practical point: a property can be above the value threshold and still avoid the surcharge if it is a primary residence. But owners should expect to prove it to the Department of Finance.

Which properties are covered?

The law potentially applies to three categories of residential property in New York City:

| Property type | Tax Class | Potentially covered? |

| One- to three-family homes, et. al | 1 | Yes, and mixed use properties too. But bungalow colonies & vacant land are excluded. |

| Residential condominium dwelling units | 2 | Yes |

| Residential cooperative dwelling units | 2 | Yes, through special co-op rules |

The law contains exclusions. The certificate of occupancy exclusion is aimed at buildings under construction: a tax class 1 or tax class 2 property is excluded if a temporary or permanent certificate of occupancy is required and has not yet been issued. The law also excludes unsold sponsor condominium and cooperative units, or units where the economic interest in the unit has not yet been transferred by the offering-plan filer. Not subject to the law: commercial properties, hotels, rental apartment buildings.

Mixed-use tax class 1 properties may be a problem area. The law applies to tax class 1 property, other than vacant land, but it does not fully explain how the surcharge should be applied where a tax class 1 property has both residential and commercial components. DOF rulemaking may help clarify how those properties will be handled.

The law has two phases

The first two tax years use current DOF-style property tax values. Later years use a different approach for condos and co-ops. For tax class 1 homes, the two phases are the same.

Phase one: tax years 2026/27 and 2027/28

For tax years beginning July 1, 2026 and July 1, 2027, the law uses “phase one market value.” For tax class 1 homes and tax class 2 residential condos, that means the DOF market value for the property. For a co-op apartment, the law imputes a value to the apartment based on the DOF market value of the co-op property and the apartment’s share allocation.

This phase-one structure is especially important for co-ops and condos. In the first two years, the condo and co-op threshold is $1 million of DOF phase-one market value, not $5 million of true “real world” market value.

| Property type | Phase-one market value | Surcharge rate |

| Tax class 1 | $5 million to $15 million | 0.8% |

| Tax class 1 | Over $15 million to $25 million | 1.05% |

| Tax class 1 | Over $25 million | 1.3% |

| Condo or co-op unit | $1 million to $3 million | 4.0% |

| Condo or co-op unit | Over $3 million to $5 million | 5.25% |

| Condo or co-op unit | Over $5 million | 6.5% |

Phase two: tax years 2028/29 through 2030/31

Beginning with tax years on and after July 1, 2028, the law switches to “phase two market value.” For tax class 1 property, DOF continues to use the DOF market value for the property. For condos and co-ops, however, the law changes the valuation approach.

Starting with the January 2028 assessment roll, DOF must publish sales-based market values for condo and co-op apartments for purposes of this surcharge. DOF will need to consider what the apartment would actually sell for, or what the apartment is really worth, rather than relying on the current rental-income-based co-op/condo valuation system used for ordinary property taxes.

In phase two, the threshold becomes $5 million for all covered property types, including condos and co-ops. The rates are 0.8%, 1.05%, and 1.3%, depending on phase-two market value.

Why the DOF value may not mean what owners think it means

For tax class 1 homes, DOF’s market value is easier for many owners to evaluate because it’s already sales-based. Owners often have a sense of what their one-, two-, or three-family home would sell for. If they bought their home recently, their purchase price could be an indicator of value. If their neighbors’ homes are comparable and have sold recently, those sales prices could be indicators of value.

For condos and co-ops, the analysis is different. DOF currently values tax class 2 co-ops and condos as if they were income-producing rental properties. That means the phase-one condo and co-op values are tied to estimated rents, expenses, capitalization rates, and income-based valuation methods, not the apartment’s hypothetical sales price.

DOF has already determined the final 2026/27 assessment market values that will be used for the first year of the surcharge. DOF published the FY2027 final assessment data on its website on May 25, 2026. Condo owners and tax class 1 owners should review their 2026/27 final DOF market values now, especially where the property is clearly not a primary residence.

DOF will issue the next tentative assessment roll on or about January 15, 2027, for tax year 2027/28 which begins July 1, 2027. For tax class 2 properties, including most condos and co-ops, the regular Tax Commission protest deadline is generally March 1. For tax class 1 properties, the regular Tax Commission deadline is generally March 15.

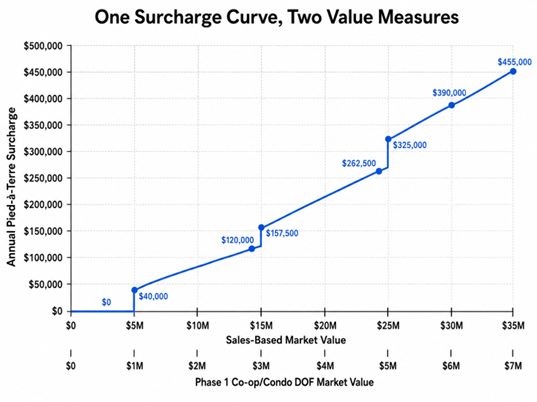

Sample surcharge amounts

The law applies the applicable rate to the full surcharge market value, rather than only to the amount over the threshold. If that reading is correct for the 2nd and 3rd tiers, the annual surcharge can be significant.

| Tax class 1 DOF market value | Phase-one rate | Approximate annual surcharge |

| $5,000,000 | 0.8% | $40,000 |

| $10,000,000 | 0.8% | $80,000 |

| $20,000,000 | 1.05% | $210,000 |

| $30,000,000 | 1.3% | $390,000 |

| Condo/co-op phase-one market value | Phase-one rate | Approximate annual surcharge |

| $1,000,000 | 4.0% | $40,000 |

| $2,000,000 | 4.0% | $80,000 |

| $4,000,000 | 5.25% | $210,000 |

| $6,000,000 | 6.5% | $390,000 |

These examples assume the property is not a primary residence and no exclusion applies.

What our initial DOF data review suggests

Our initial review of DOF final assessment data suggests that the potential surcharge base is concentrated among a relatively small number of high-value properties and buildings. These figures assume that every property above the threshold is not a primary residence. Actual liability will be lower because some properties will be primary residences, some may qualify for an exclusion, and some owners may challenge the value or the primary-residence determination.

Residential condo lots

| Metric | Initial finding |

| Tax class 2 individual residential condo lots in NYC | Approximately 231,000 |

| Condo lots with DOF market value of at least $1 million | Approximately 11,800 |

| Share of individual residential condo lots above $1 million | 5.1% |

| Total potential phase-one surcharge if all are non-primary residences | $818 million |

| Condo properties containing those 11,800 units | Approximately 1,500 |

| Top 20% of those condo properties | 300 properties: $565 million, or 69% of potential condo surcharge |

| Top 20% of those condo units | 2,360 units: $321 million, or 39% of potential condo surcharge |

In the top 100 condo units by potential surcharge exposure, 73 appear to be owned by a non-natural-person record owner, such as an LLC, corporation, trust, or trustee, based on the DOF owner-name field. Twenty-five appear to be directly owned by natural persons. The remaining two did not clearly fit either category from the DOF owner-name field. Record ownership is not the same thing as beneficial ownership or primary residence status, but it does show why entity ownership and proof of primary residence will be important issues.

Tax class 1 properties

| Metric | Initial finding |

| Tax class 1 properties reviewed | Excluding vacant land and bungalow colonies |

| Tax class 1 properties with DOF market value of at least $5 million | Approximately 6,800 |

| Total DOF market value of those properties | Approximately $60 billion |

| Geographic concentration by market value | 62% Manhattan; 36% Brooklyn |

| Total potential phase-one surcharge if all are non-primary residences | $537 million |

| Geographic concentration by potential surcharge | 66% Manhattan; 32% Brooklyn |

| Area concentration | Approximately half of all surcharge will come from the Upper East Side and Greenwich Village/SoHo areas |

| Top 20% of properties | 1,360 properties: $249 million, or 46% of potential tax class 1 surcharge |

Primary residence will be the central issue

The surcharge applies only if the property is not a primary residence. Under the law, primary residence is tested as of the taxable status date immediately preceding the fiscal year in which the surcharge is imposed. The Tax Law portion of the statute defines that taxable status date as January 5. The NYC fiscal year runs July 1 to June 30.

For tax year 2026/27, the relevant date is January 5, 2026. For tax year 2027/28, the relevant date is January 5, 2027.

A property may qualify as a primary residence if it is used as the primary residence of one or more covered owners, or an immediate family member of one or more covered owners, provided the covered owners are natural persons. Immediate family member means spouse, child, sibling, parent, grandparent, or grandchild.

A property may also qualify if it is used as the primary residence of a natural-person tenant or qualifying subtenant occupying under a bona fide, arm’s-length lease with a term of at least one year.

Properties owned by LLCs, corporations, partnerships, and trusts require careful review. Entity ownership does not automatically mean the surcharge applies. But an entity itself cannot live in a property, and the law requires the relevant covered owner whose residence is being relied upon to be a natural person.

Owners should be careful before claiming that a New York City property is their primary residence. That position may have New York State and New York City personal income tax consequences.

DOF notices and key dates

DOF must make an annual initial determination that threshold-value covered properties are not primary residences, based on information available to DOF and factors that DOF may specify by rule. The law specifically allows DOF to consider whether the property was occupied for a majority of days during a calendar year.

For the first year, DOF must provide the initial non-primary-residence notice no later than August 30, 2026. The notice must give the owner an opportunity to submit proof of primary residence. DOF may require certifications and documentation, including tax-return address evidence, STAR evidence, proof of tenant occupancy, or proof that an immediate family member uses the property as a primary residence.

The first surcharge payment for tax year 2026/27 is due January 1, 2027, the same date as the second semiannual installment of New York City real property taxes.

| Dates (estimated) | What happens |

| May 25, 2026 | DOF published FY2027 final assessment data; owners can review final 2026/27 DOF market values. |

| May 28, 2026 | Governor signed A10009C into law. |

| July 1, 2026 | First tax year covered by the surcharge begins. |

| August 30, 2026 | Deadline for DOF to issue first-year initial non-primary-residence notices. |

| January 1, 2027 | First year surcharge payment is due for tax year 2026/27. |

| January 15, 2027 | Expected tentative assessment roll date for tax year 2027/28. |

| March 1, 2027 | Regular Tax Commission deadline for tax class 2 properties, including most condos and co-ops. |

| March 15, 2027 | Regular Tax Commission deadline for tax class 1 properties. |

| July 1, 2027 | Second year surcharge payment is due for tax year 2027/28 (1st half). |

| January 1, 2028 | Second year surcharge payment is due for tax year 2027/28 (2nd half). |

| January 15, 2028 | DOF begins publishing sales-based condo/co-op values for phase two surcharge purposes, applicable for tax years 2028/29 and later. |

Owners may need to protest value, primary residence, or both

The law creates a separate Tax Commission review process for the surcharge. The grounds for review are that the surcharge market value is excessive, that it is unlawful, or that the property or co-op apartment is a primary residence.

This review process is separate from an ordinary property tax protest. An owner should not assume that a regular Tax Commission protest automatically preserves surcharge-specific issues.

For tax year 2026/27, the filing window is unusual. The law allows an application to be filed beginning when DOF issues the notice of surcharge, and continuing until the last date for filing a surcharge market-value review application for tax year 2027/28.

If a property is definitely not a primary residence, the owner should consider being ready to protest the value. For tax class 1 properties, that may involve reviewing whether DOF’s market value is supported by sales of comparable homes. For condos and co-ops in phase one, the valuation issue will be harder because the current DOF values are based on estimated rental income rather than apartment sale prices.

Because the surcharge review process is valuation-heavy, owners should consider using a representative who understands New York City property valuation, who regularly appears before the New York City Tax Commission, and who can file Article 7 petitions if court review becomes necessary.

I am an attorney who solely focuses on New York City real estate tax issues. I am also a former appraiser and remain an Accredited Senior Appraiser of the American Society of Appraisers. Our property tax team has appeared before the New York City Tax Commission thousands of times and regularly files Article 7 petitions in Supreme Court challenging New York City property taxes.

What co-op boards and managing agents should do now

Co-ops may face the most administrative burden. For phase one, DOF will not value each co-op apartment by sales price. Instead, the law imputes value to a co-op apartment using the co-op building’s DOF market value and the apartment’s share allocation.

DOF will send the non-primary residence determination Notices to the co-op or managing agent, who should then notify the affected shareholder. If a surcharge is imposed on a co-op apartment, DOF adds the surcharge to the co-op property’s statement of account. The co-op corporation must then collect the unit-specific surcharge from the affected tenant-stockholder.

Co-op managing agents should start preparing a schedule of units, shares, total shares, and potentially affected apartments. They should also be prepared to handle DOF notices, forward notices to affected shareholders, and address billing procedures if a surcharge appears on the co-op’s tax account.

Boards should not wait until the surcharge appears on a bill to decide how notices, shareholder inquiries, payment, protests, and refunds will be handled.

What condo boards and managing agents should do now

Condos are less complicated than co-ops for this purpose because each condo unit is separately assessed and separately billed. In most cases, the surcharge should be a unit-owner issue rather than a board collection issue.

That does not mean condominium managing agents can ignore the law. Unit owners will likely ask questions about DOF values, primary residence, entity ownership, tenant occupancy, and protest rights. Condo managing agents should be prepared to refer unit-owner inquiries to a representative familiar with New York City property valuation and Tax Commission procedure.

Condo boards and managing agents should avoid becoming responsible for determining a unit owner’s personal tax residency, reviewing private income tax records, or advising whether an owner should claim New York City primary residence.

Next steps

Affected owners, boards, and managing agents should begin preparing now. The first DOF notices are due by August 30, 2026, and the first surcharge payment is due January 1, 2027.

- Review the 2026/27 final DOF market value for the property or unit.

- Determine whether the property is clearly a primary residence, clearly not a primary residence, or uncertain.

- Review ownership structure, including LLCs, corporations, partnerships, and trusts.

- Review leases if the property is tenant-occupied.

- Gather records that may support primary residence where appropriate.

- If the property is not a primary residence, consider whether the DOF value should be reviewed or challenged.

- For co-ops, prepare a unit/share schedule and a process for notices and billing.

- For condos, prepare to route unit-owner inquiries to a qualified representative.

Conclusion

The new pied-à-terre surcharge is more than a simple tax on second homes. It raises questions about primary residence, entity ownership, tenant occupancy, valuation, DOF notices, Tax Commission review, Article 7 review, and co-op and condo administration.

Owners of potentially affected properties should not wait until the surcharge appears on a tax bill. The first step is to review the property’s DOF market value and determine whether the property may be treated as a non-primary residence. If the property is definitely not a primary residence, the next step may be to prepare for a valuation review and possible Tax Commission challenge.

Because DOF rules have not yet been issued, some details remain open. But the law is now enacted, the first notices are due in three months, and property owners, boards, and managing agents should begin preparing now.

Prior Coverage

My blog posts:

- NYC Pied-a-Terre Tax Proposal Will Force a New Way to Value Co-ops and Condos

- NYC Executive Budget Update: The “Last Resort” Property Tax Rate Increase Is Gone – But Property Tax Bills Are Still Projected to Rise

- An Outside-NYC Pied-à-Terre Tax Bill May Preview Key Issues for a Future NYC Version

I was interviewed by, quoted in, or cited by the Media:

- Hochul’s pied-à-terre tax proposal raises questions over how NYC assesses value of ultra-luxury real estate – ABC7 New York

- New York approves pied-à-terre in state budget. – Crain’s New York Business

- Hochul’s Pied-à-terre Tax Lays Enforcement On Co-ops – The Real Deal

- The Pied-à-Terre Tax and Its Potential Revenues – Office of the New York City Comptroller Mark Levine (footnote 5)

- New York’s new pied-à-terre tax is a concern for co-ops | Habitat Magazine, New York’s Co-op and Condo Community

- Would Donald Trump have to pay the NYC pied-à-terre tax? – Gothamist

- Pied-à-Terre Tax: More Questions than Answers for Co-ops – The Real Deal

- Hedge fund Citadel bets on Miami as debate over New York second homes heats up | Reuters

Source note

This article is based on Part HH of A10009C, which added New York Tax Law Article 30-C and New York City Administrative Code Chapter 32. The statistical figures described above are based on our initial review of NYC Department of Finance final assessment data and assume, for illustration, that all threshold properties are non-primary residences. Actual surcharge liability will depend on primary-residence status, statutory exclusions, DOF rules, valuation review, and owner-specific facts.

This article covers the major changes in the State law that may be of interest to our readers. It is not intended to be a complete review of all provisions of the new law. The law may change.

This blog is a form of attorney advertising. We provide this information as a service to our clients and other readers for educational purposes only. Nothing in this blog should be construed as, or relied upon, as legal advice or as creating a lawyer-client relationship.