NYC Property Tax

NYC Pied-a-Terre Tax Proposal Will Force a New Way to Value Co-ops and Condos

Published 5/15/2026 at 2:10 PM

By: Benjamin M. Williams

Note: Details were still being reported as of May 14-15, 2026, and the final bill should be reviewed when released. This post is based on the reported proposal, current New York City property tax valuation rules, and preliminary analysis of potential properties that may meet the reported market value thresholds.

New York City’s proposed pied-a-terre tax is being described as a tax on high-value second homes. But the more significant long-term issue may be valuation: the proposal will require the New York City Department of Finance (DOF) to begin estimating the sales value of co-op and condo apartments, which is not how those properties are valued for regular property tax purposes today.

Under the proposal reported this week, the surcharge would apply to certain non-primary residences in one- to three-family homes, co-ops, and condos. The tax is intended to raise approximately $500 million annually for New York City. The City Comptroller has warned, however, that actual revenue could be lower depending on exemptions, enforcement, rental treatment, ownership structures, and owner behavior.

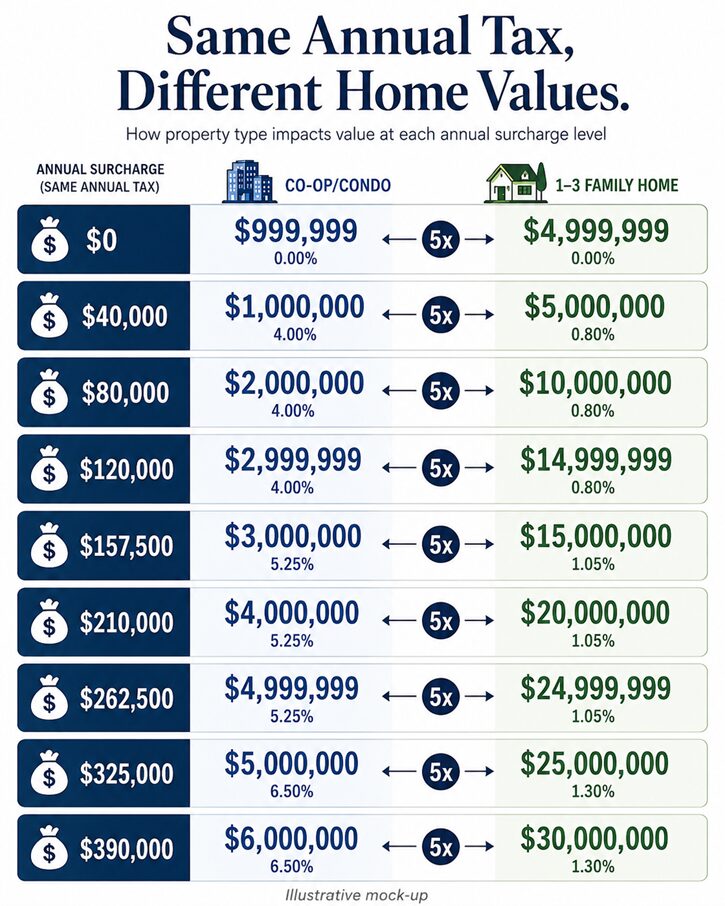

Because the proposed rates do not appear to be tiered, the surcharge could jump sharply when a property crosses a valuation threshold, even by $1. For example, a condo valued at $3,000,000 would owe a $157,500 surcharge, while a condo valued at $2,999,999 would owe approximately $120,000 — a roughly $37,500 difference based on a $1 valuation change. This impact will make it especially important for property owners to protest their market values.

Reported Pied-a-Terre Tax Rate Schedule

The proposal uses a two-step approach for co-ops and condos. One- to three-family homes would be taxed immediately based on DOF’s estimated market value, which is already based on comparable sales. Co-ops and condos would initially be taxed using DOF’s current market value, which is based on rental income methodology. After the first two years, DOF would move to a sales-based valuation system for co-ops and condos for purposes of the surcharge.

| Property type / timing | Value used | Reported value bracket | Reported surcharge rate | Example annual surcharge |

| Co-ops and condos – first two years | Current DOF market value based on estimated rental value | $1 million to $3 million | 4.00% | $1 million x 4.00% = $40,000 |

| Co-ops and condos – first two years | Current DOF market value based on estimated rental value | More than $3 million to $5 million | 5.25% | $4 million x 5.25% = $210,000 |

| Co-ops and condos – first two years | Current DOF market value based on estimated rental value | $5 million or more | 6.50% | $5 million x 6.50% = $325,000 |

| One- to three-family homes – immediately | DOF market value based on comparable sales | $5 million to $15 million | 0.80% | $10 million x 0.80% = $80,000 |

| One- to three-family homes – immediately | DOF market value based on comparable sales | More than $15 million to $25 million | 1.05% | $20 million x 1.05% = $210,000 |

| One- to three-family homes – immediately | DOF market value based on comparable sales | More than $25 million | 1.30% | $30 million x 1.30% = $390,000 |

| Co-ops and condos – after first two years | New DOF sales-based valuation | Same as one- to three-family homes | 0.80% / 1.05% / 1.30% | Based on new sales-based value |

Source note: Rate details are based on May 14, 2026 reporting by the New York Times and NY1. The final statute should be reviewed before relying on exact bracket lines, definitions, or exemptions.

Why the Co-op and Condo Threshold Is So Important

For tax class 1 one- to three-family homes, DOF already estimates market value using sales of similar properties in similar neighborhoods. But tax class 2 co-ops and condos are different. DOF values them as if they were income-producing rental properties, using income and expense information from comparable rental buildings.

That means the term “market value” can be misleading for co-ops and condos. A luxury condo that could sell for many millions of dollars may have a much lower DOF market value because DOF is not directly estimating what a buyer would pay for that apartment. One reported example described a condominium with an $18.5 million sales value but only a $1.1 million DOF market value. Under the temporary two-year system, that unit would pay a surcharge of approximately $44,000.

Using our rough analysis, a $1 million DOF market value condo apartment may imply an estimated rental value of approximately $17,000 per month. At a 45% assessment ratio, that apartment would have an assessed value of $450,000. Using a 12.44% tax rate for illustration, the regular property tax would be approximately $56,000. A 4% pied-a-terre surcharge would add $40,000, bringing the total annual property tax burden to approximately $96,000.

DOF Has Already Been Testing Sales-Based Condo Valuation

The proposal’s two-year transition period is important because DOF would need to build a new valuation system for co-ops and condos. In March 2025, DOF entered into a six-month demonstration project with C3 AI to explore using artificial intelligence to value residential condominium properties using machine learning, sales data, and market data. The City Record notice described the pilot as studying the feasibility of using the sales comparison approach for condominiums with more than 10 units.

That pilot reportedly did not change current condo assessments. But it shows that the City has already been exploring the technical problem that this pied-a-terre proposal would now make more immediate: how to estimate the sales value of individual condominium apartments at scale.

Is This a Preview of Property Tax Reform?

The pied-a-terre tax could also be a step toward broader property tax reform. The New York City Advisory Commission on Property Tax Reform recommended creating a new expanded residential class that would include one- to three-family homes, co-ops, condos, and four- to ten-unit rental buildings. It also recommended valuing all properties in that new residential class using a sales-based methodology, which would end the current requirement to value co-ops and condos based on comparable rental buildings. Both changes would require State legislation.

If DOF builds a sales-based co-op and condo valuation system for the pied-a-terre tax, that same infrastructure could potentially be used later for broader property tax reform. That does not mean regular co-op and condo property taxes would immediately change. But it would move the City closer to having the data and administrative process needed to replace rental-based co-op and condo valuations.

The political backdrop also matters. Mayor Zohran Mamdani said earlier this year that a New York City property tax reform proposal would be released, but no comprehensive proposal has yet been released. The pied-a-terre tax may therefore become the first practical step toward changing how high-value owner-occupied residential properties are valued.

Preliminary Revenue Analysis

We reviewed potential properties that appear to meet the reported market value thresholds before determining which properties would qualify for any primary residence, family member, rental, or other exclusion.

| Property category | Preliminary universe identified | Potential pied-a-terre tax revenue |

| Residential condominium units | 11,684 units over $1 million DOF market value | $809 million |

| Co-op apartments | 456 co-op buildings containing 5,244 apartments | $304 million |

| Tax class 1 one- to three-family homes | 3,508 tax lots containing 3,944 units | $351 million |

| Total | Approximately 20,872 units / homes | $1.464 billion |

These numbers are before excluding primary residences and other potentially exempt properties. If the City’s target is $500 million per year, then roughly one-third of the notional universe – about 7,000 units or homes – would need to remain taxable after exclusions. In that scenario, the average pied-a-terre tax would be approximately $70,000 per apartment or home per year.

We had to make several assumptions and adjustments to estimate which co-ops and tax class 1 properties might be taxable, based on average market value per unit. For example, a four-unit co-op with a $3 million market value wouldn’t be included in our potential universe, because the average market value is less than $1 million per unit. Nevertheless, that co-op could have two apartments with a rental-based market value of $1 million each and the other two with $500,000 each – and the former two would be taxable and the latter two not taxable.

The City Comptroller’s analysis similarly emphasized that the revenue estimate depends heavily on unresolved implementation questions, including primary residence determinations, rental exemptions, co-op and condo valuation, treatment of two- and three-family homes, LLC and trust ownership, and behavioral responses.

Key Questions Still Unanswered

How will co-ops be valued? Condos already have separate tax lots, but co-ops generally do not. The co-op corporation receives one assessment for the entire building. Will DOF value the entire building and allocate value by shares? Will it value only the residential component? What happens if a co-op has valuable commercial space? Or will DOF attempt to value each apartment separately?

How will primary residence be determined? The City could use the existing co-op/condo abatement process, where managing agents report primary residence information. It could also use NYC or New York State income tax records. The choice matters because it will affect audit burden, administration, privacy, and the number of appeals.

How will LLCs, trusts, and family-use apartments be handled? Luxury apartments are often owned through LLCs or trusts. Those structures may not neatly identify a primary resident, even when the apartment is used as someone’s home. The proposal reportedly includes an exemption for apartments bought for certain family members, but the mechanics of that exemption remain unclear.

How will owners protest the market value? This may become one of the most important practical issues. The FY2027 Tax Commission filing deadlines have already passed: March 2, 2026 for tax classes 2, 3, and 4, and March 16, 2026 for tax class 1. DOF has a separate Request for Review process for market value, but the FY2027 deadlines for that process have also passed. If the new surcharge depends on market value, affected owners will need a clear process to challenge that value.

Can the Tax Commission handle a wave of individual unit protests? Condo buildings often file Tax Commission applications together for residential units. If individual condo owners have a new surcharge tied to their own unit value, some owners may want to file separately. Tax class 1 owners also rarely protest because assessed value caps often make DOF market value less important. A new surcharge could change that behavior.

Will one-year valuation spikes trigger the tax? Earlier pied-a-terre proposals discussed by the Comptroller used a five-year average market value for one- to three-family homes. The currently reported proposal does not appear to use a five-year average for all categories. If the final bill does not include a smoothing mechanism, a one-year valuation error or spike could immediately trigger a large surcharge.

Will sponsors and developers be taxed on unsold condo units? New condo buildings often take several years to sell out. If unsold sponsor units are treated as non-primary residences, the tax could increase carrying costs during sellout. The proposal will need to address whether sponsor-owned units are taxable, exempt, or treated differently.

Conclusion

The pied-a-terre tax is not just a proposed surcharge on high-value second homes. It will require New York City to create a new sales-based valuation system for co-ops and condos. That would be a major change from the current property tax system, where co-ops and condos are generally valued as if they were rental buildings.

The first two years may be the temporary phase. The longer-term issue is whether this becomes the starting point for a broader shift in how New York City values owner-occupied residential property.

This blog is a form of attorney advertising. We provide this information as a service to our clients and other readers for educational purposes only. Nothing in this blog should be construed as, or relied upon, as legal advice or as creating a lawyer-client relationship.