NYC Property Tax

NYC Executive Budget Update: The “Last Resort” Property Tax Rate Increase Is Gone – But Property Tax Bills Are Still Projected to Rise

Published 5/13/2026 at 7:40 AM

By: Benjamin M. Williams

On May 12, 2026, the Mayor released New York City’s Fiscal Year 2027 Executive Budget. For property owners, the headline is that the Administration has scrapped the “last resort” 9.5% property tax rate increase that appeared in the February Preliminary Budget. The Mayor’s materials now describe the budget as balanced “without raising property taxes,” and the budget presentation uses the even cleaner phrase: “No Property Tax Increase.”

That is good news, but it requires a little property-tax translation.

The Executive Budget does not eliminate property tax growth. It eliminates the proposed increase to the City’s overall property tax rate, which would have moved from 12.283% to 13.450%. The City’s own Financial Plan says that reversing that rate increase reduces expected revenue by $3.7 billion in FY2027.

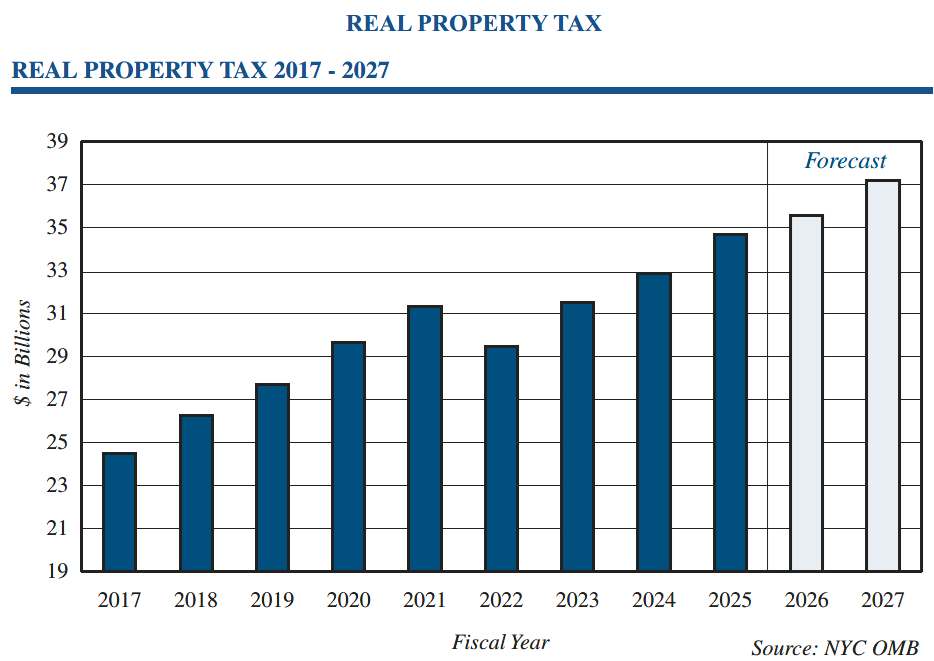

But the same Financial Plan also projects that real property tax revenue will increase from $35.536 billion in FY2026 to $37.187 billion in FY2027. That is a 4.6% increase. And from FY2028 through FY2030, real property tax revenue is expected to grow by an average of 2.8% per year.

So the more accurate statement is this: there is no proposed increase to the overall property tax rate, but property tax revenue — and many individual property tax bills — are still expected to increase.

What changed from the February Preliminary Budget?

In my prior post, “NYC’s Feb. 17, 2026 Preliminary Budget and the Proposed ‘Last Resort’ Property Tax Rate Increase: What It Could Mean for Taxpayers,” I discussed the Preliminary Budget’s proposed 9.5% increase to the average property tax rate.

The February Plan would have increased the average property tax rate from 12.283% to 13.450% beginning in FY2027. The City projected that the higher rate would generate $3.7 billion in FY2027, $3.6 billion in FY2028, $3.7 billion in FY2029, and $3.8 billion in FY2030. Under that plan, real property tax revenue was projected to rise to $40.349 billion in FY2027, a 14.1% increase over FY2026.

That part is now gone.

The Executive Budget reverses the proposed rate increase, reducing the FY2027 revenue forecast by $3.7 billion compared with the February Plan.

But that does not return taxpayers to a “no increase” world. It returns taxpayers to an assessment-growth world.

Why does the FY2027 increase now show 4.6%, not 3.7%?

One notable detail is that, after removing the 9.5% rate increase, the property tax growth number is actually higher than the baseline discussed in the February materials.

Under the February Plan, real property tax revenue was projected at $40.349 billion for FY2027. Removing the $3.7 billion rate increase gets to roughly $36.649 billion — about a 3.7% increase over the February FY2026 estimate of $35.361 billion.

The Executive Budget now forecasts $37.187 billion in FY2027 real property tax revenue. The reason is that the City has re-estimated the underlying property tax forecast upward. The Executive Budget identifies a positive re-estimate of FY2027 property taxes of $538 million, and it also increases the FY2026 real property tax estimate by $175 million compared with the February Plan.

The City also now expects citywide taxable billable assessed value to grow 5.1% in FY2027, slightly higher than anticipated in February. The projected FY2027 TBAV growth rates are 3.6% for Class 1, 5.3% for Class 2, 7.1% for Class 3, and 4.7% for Class 4.

In other words, the “last resort” rate increase is gone, but the roll is still growing.

Rate increases are not the only way tax bills go up

This is a key distinction for taxpayers.

A property tax bill is not driven only by the tax rate. The Department of Finance calculates the bill by multiplying taxable value by the tax rate. DOF also values and assesses property each year, and the assessment process varies by tax class.

That means a taxpayer’s bill can increase even if the applicable tax rate does not increase. A growing assessment, the phase-in of prior-year assessment increases, changes in exemptions or abatements, or changes in taxable billable assessed value can all produce higher taxes.

It is also worth remembering that the 12.283% number is not the actual tax rate used for each of the four tax classes. NYC properties are divided into four tax classes: Class 1 generally includes one- to three-family residential properties; Class 2 includes larger residential properties, including co-ops, condos, and apartment buildings; Class 3 and Class 4 are mostly utility and commercial properties.

Each class has its own tax rate. For tax year FY2026, DOF lists the rates as 19.843% for Class 1, 12.439% for Class 2, 11.108% for Class 3, and 10.848% for Class 4.

The Citywide rate is an overall, legislatively determined rate used to calculate the overall property tax levy. The class tax rates are then established by dividing each class’s levy by that class’s taxable billable assessed value.

So when the Executive Budget says the rate is being “reduced back down to 12.283 percent,” that does not mean every class rate is frozen, and it does not mean every taxpayer’s bill is flat.

Enter the new High Value Property Surcharge — the pied-à-terre tax

The Executive Budget also adds a new property-related revenue proposal: a non-resident-owned High Value Property Surcharge, commonly referred to as a pied-à-terre tax.

The Financial Plan describes this as a new property tax surcharge on high-value non-primary homes, expected to take effect beginning in FY2027. It would apply to the market value of eligible Class 1 and residential Class 2 properties — including condo and co-op units — valued over $5 million. The rate has not yet been determined. The City expects the surcharge to generate $500 million annually from FY2027 through FY2030. Nevertheless, the Comptroller expects under $400 million of revenue, as you can see in his Report where he footnoted my blog post, The Pied-à-Terre Tax Is Back: What the Bills Say, What Changed, and What Albany Still Has to Fix. (You can also see my follow-up blog post, An Outside-NYC Pied-à-Terre Tax Bill May Preview Key Issues for a Future NYC Version.)

Note the dichotomy: the City is saying “no property tax increase” while also proposing a new property tax surcharge on certain high-value, non-primary residences.

The City’s own budget materials classify the High Value Property Surcharge as a new tax program that was not included in the February Plan, and the Financial Plan states that these assumed actions are not yet incorporated into the individual tax forecasts.

So for affected taxpayers, the practical takeaway is not “no property tax increase.” It is: no broad 9.5% rate increase, but ordinary property tax growth continues — and a new surcharge may apply to certain high-value non-primary residences.

Other property tax items to watch

There are a few additional items in the Executive Budget that deserve attention from property owners, managers, co-op and condo boards, and tax professionals.

First, the Financial Plan includes $13 million in City savings associated with Department of Finance measures to increase co-op/condo abatement compliance. That likely means more scrutiny of abatement eligibility and potentially more denials, revocations, or documentation requests.

Second, DOF enforcement around required filings remains an issue to watch. The Financial Plan notes that DOF assesses penalties for failure to timely file Real Property Income and Expense statements, and that enforcement efforts are expected to improve compliance due to increased penalties for non-filers who have not filed for three consecutive years.

Third, the State budget process still matters. The City’s Executive Budget discusses cost increases reflected in the FY2027 Preliminary Budget that would be imposed by the Governor’s Executive Budget, including an increase in the J-51 property tax exemption from 70% to 100% of certified reasonable costs. But the City also cautions that the Governor’s proposed Executive Budget remains subject to negotiations with the State Senate and Assembly, and that there is no assurance that the actions described will be enacted as proposed.

Conclusion

The Mayor’s Executive Budget is a materially better outcome for broad-based property taxpayers than the February Preliminary Budget. The proposed 9.5% “last resort” rate increase appears to be off the table.

But the phrase “no property tax increase” is too broad.

The better reading is:

- No increase to the overall property tax rate.

- No broad 9.5% rate hike.

- But real property tax revenue is still projected to grow 4.6% from FY2026 to FY2027, assessment growth is still driving higher revenues, and a new $500 million-per-year pied-à-terre surcharge is now part of the budget plan.

For taxpayers, the next items to watch are the final roll, class shares, final class tax rates, the details of the pied-à-terre surcharge, and DOF enforcement activity around abatements and RPIE filings.

This blog is a form of attorney advertising. We provide this information as a service to our clients and other readers for educational purposes only. Nothing in this blog should be construed as, or relied upon, as legal advice or as creating a lawyer-client relationship.