NYC Property Tax

NYC’s Feb. 17, 2026 Preliminary Budget and the Proposed “Last Resort” Property Tax Rate Increase: What It Could Mean for Taxpayers

Published 2/17/2026 at 10:51 AM

By: Benjamin M. Williams

On February 17, 2026, Mayor Mamdani released New York City’s FY 2027 Preliminary Budget. One of the most discussed items is a proposed “last resort” property tax rate increase, described as a contingency if other revenue options are not adopted.

This post is not about politics. It is about how a rate increase works mechanically in NYC, how it can translate into actual dollars on a bill, and what property owners may want to keep in mind during the current tax protest season.

The “last resort” increase is not a percentage-point increase

When people hear “+9.5%,” it is easy to assume the tax rate jumps by 9.5 percentage points. That is not what this means.

A “+9.5%” rate increase is a multiplier applied to the existing rate. Based on the numbers the Mayor provided, it effectively calculates out to about +10.1% for FY 2027. If we use 10% as a simple illustration, the math looks like this:

- Tax Class 1 (i.e, Residential properties under 4 units)

- FY 2026 rate: 19.843%

- +10% example: 19.843% × 1.10 = 21.8%

- Tax Class 2 (i.e, Residential properties over 3 units)

- FY 2026 rate: 12.439%

- +10% example: 12.439% × 1.10 = 13.7%

- Tax Class 4 (i.e., Commercial properties)

- FY 2026 rate: 10.848%

- +10% example: 10.848% × 1.10 = 11.9%

In practical terms:

- If you expected to pay $10,000 in property taxes, you’d pay about $11,000 instead.

- If you expected to pay $100,000, you’d pay about $110,000 instead.

Baseline growth plus the “last resort” increase

There is another layer that matters: before adding in the “last resort” increase, real property tax revenue was expected to increase +3.6% in FY 2027.

For additional context, here is how the Mayor’s property tax revenue forecast describes the FY 2027 property tax assumptions:

- Real property tax (RPT) revenue is forecast at $35.361 billion in 2026, growth of 2.1 percent over the prior year, and an increase of $140 million from the November 2025 Plan, as collections fiscal year-to-date have been higher than plan.

- In 2027, property tax revenue is revised up by $3.825 billion to $40.349 billion, growth of 14.1 percent, reflecting the assessed value growth seen in the Department of Finance (DOF)’s tentative roll as well as an increase in real property tax rates from 12.283 percent to 13.450 percent.

- The higher property tax rates are anticipated to generate $3.7 billion in FY 2027, $3.6 billion in 2028, $3.7 billion in 2029 and $3.8 billion in 2030.

- The levy projection for 2027 is based on the updated tax rates and the 2027 tentative roll, which the Department of Finance released on January 15th, 2026.

- Values from the tentative roll are then adjusted to reflect processes taking place between the tentative and final roll publication including Tax Commission actions, Department of Finance changes by notice, and the completion of exemption processing.

When that baseline growth is combined with the 10.1% increase, the total change from FY 2026 to FY 2027 is +14.1%.

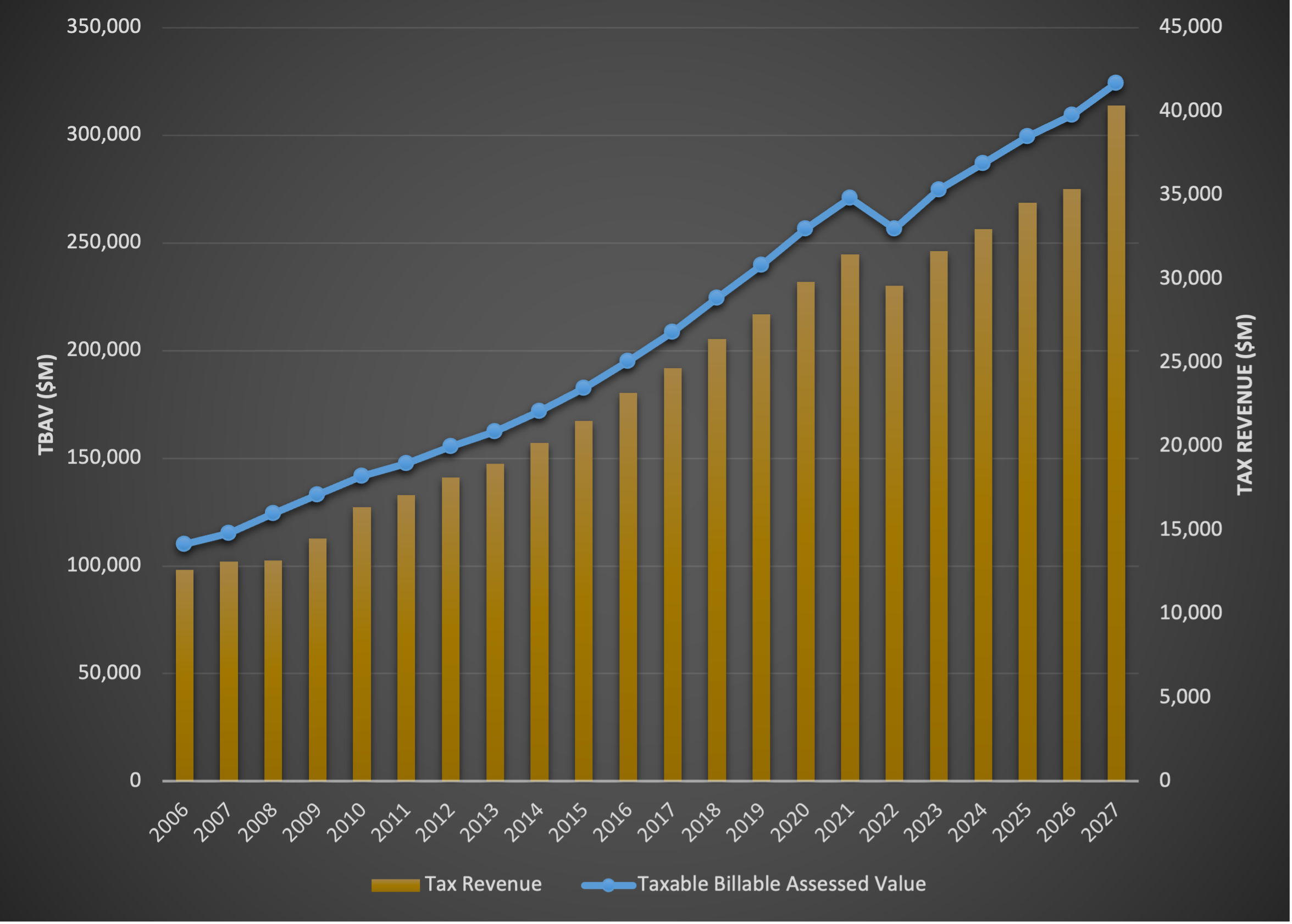

The forecast also puts some FY 2027 numbers around taxable billable assessed value growth by class:

- In the final roll estimates, Class 1 taxable billable assessed value (TBAV) is expected to be $28.355 billion, growth of 3.6 percent over 2026, and is forecast to grow at an annual average of 3.6 percent from 2028 through 2030.

- The final roll estimate of Class 2 TBAV is expected to be $126.541 billion, growth of 5.9 percent over 2026.

- Class 2 growth in 2027 is led by rental properties, although regulated rental properties growth is more subdued.

- Finally, the final roll estimate of Class 4 TBAV is expected to be $140.237 billion, growth of 4.7 percent over 2026.

- Out-year growth in Class 4 is expected to stay subdued in later years attributable to continued weakness in the office market.

- Citywide, total TBAV is expected to increase by 4.8 percent in 2027 to $324.130 billion.

Using my example:

- If you paid $100,000 last year, expect roughly $114,100 this year (using the combined +14.1% figure).

What City Hall often means by “we haven’t raised property taxes since 2009”

There is a statement that appears frequently in public discussions: that the City “hasn’t raised property taxes since 2009.”

What that typically refers to is the overall (blended) property tax rate – an aggregate figure across all four tax classes. It is not the rate any taxpayer actually pays. In NYC, taxpayers are billed under four separate tax class rates, and those class rates vary over time.

At the same time, the property tax levy / revenue can still rise even if the blended rate appears flat, because the tax base grows. In NYC, the biggest driver is the growth in taxable billable assessed value, which increases as market values rise and as properties change, improve, or trade at higher prices.

The long-term figures are:

- Since FY 2006, taxable billable assessed value has increased on average +5.3% per year.

- That growth is driven by average citywide market value increases of +5.0% per year.

- Property tax revenue has increased on average +5.8% per year over the same time.

So two things can be true at once: the City can say the “overall rate” has not meaningfully increased, while many taxpayers still experience higher bills over time due to growth in the taxable base.

Why a rate increase matters for valuation and tax protests

From a valuation standpoint, a meaningful property tax rate increase is not just a budgeting headline – it can show up in the numbers that drive market value.

Higher property taxes generally mean higher operating expenses, which can reduce net operating income (NOI). For income-producing property, lower NOI tends to support a lower market value conclusion (all else equal). That can create a strategic path to arguing for approximately -4% market value reductions, where the economics support it – because the property’s stabilized expense load is higher.

That is not a guarantee, and it depends heavily on the property type, the leases (including tax escalations), expense recoveries, and the income/expense profile. But as a valuation concept, the connection is straightforward: higher taxes → higher expenses → lower NOI → lower value.

If the city does pass a tax rate increase, we will be aggressively arguing for reductions in our clients’ assessed values.

Timing note: Tax Commission filing season is here

Whatever happens in the budget process between now and July 1st, the Tax Commission calendar is not waiting. Tax Commission applications are due Monday, March 2, 2026, and we are very busy helping clients evaluate their positions and file timely applications. You cannot wait until after the city decides to increase the tax rate to decide if you’re going to file a protest; you must do so preemptively.

If you are assessing budget impact for FY 2027, it may be helpful to run scenarios that separate:

- baseline growth in value (what would have happened absent a rate increase), and

- the incremental impact of the proposed “last resort” multiplier.

That way, you can understand whether a change is being driven by the value, the rate, or both – and plan accordingly.