NYC Property Tax

Rent-Stabilized Multifamily Values Are Down. Property Tax Assessments Need to Catch Up.

Published 4/24/2026 at 6:20 PM

By: Benjamin M. Williams

New York City’s rent-stabilized multifamily market is no longer being valued on the growth assumptions that supported pricing before 2019. For property tax purposes, that matters.

Class 2 apartment buildings are supposed to be valued as income-producing property. For larger rental buildings, the New York City Department of Finance uses income and expense information, estimates current net income, and applies a capitalization rate to determine market value. Once market value is determined, Class 2 assessed value is generally calculated at 45% of market value. In other words, if the income stream has been permanently impaired, the assessment should be scrutinized carefully.

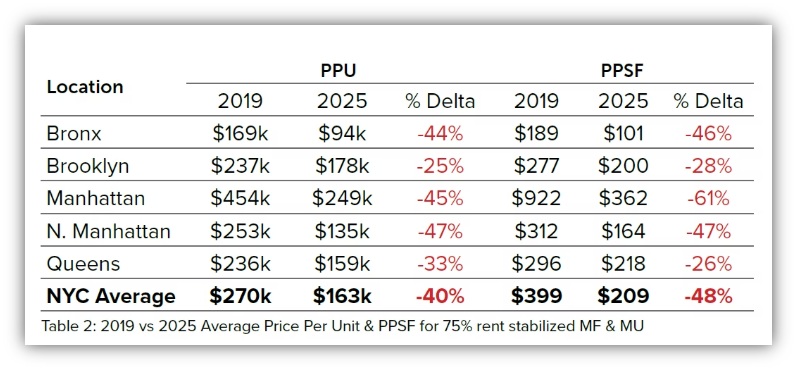

The sales market is already sending that signal. Ariel Property Advisors’ 2025 Multifamily Year in Review shows that buildings with 75% or more rent-stabilized units have suffered a major decline in value since 2019. Citywide, average price per unit fell from $270,000 in 2019 to $163,000 in 2025, a 40% decline. Average price per square foot fell from $399 to $209, a 48% decline. The decline was not isolated to one borough: Manhattan price per square foot fell 61%, Northern Manhattan price per unit fell 47%, and Bronx price per unit fell 44%.

Source: New York City 2025 Multifamily In Review Report by Ariel Property Advisors

This is not simply a “quiet market” or a temporary lack of transaction volume. The issue is that the basic economics of rent-stabilized ownership have changed. Ariel attributes the distress to the combined effect of HSTPA, rising expenses, and mortgage maturities at higher rates, all of which have continued to drive non-discretionary sales in the rent-stabilized segment.

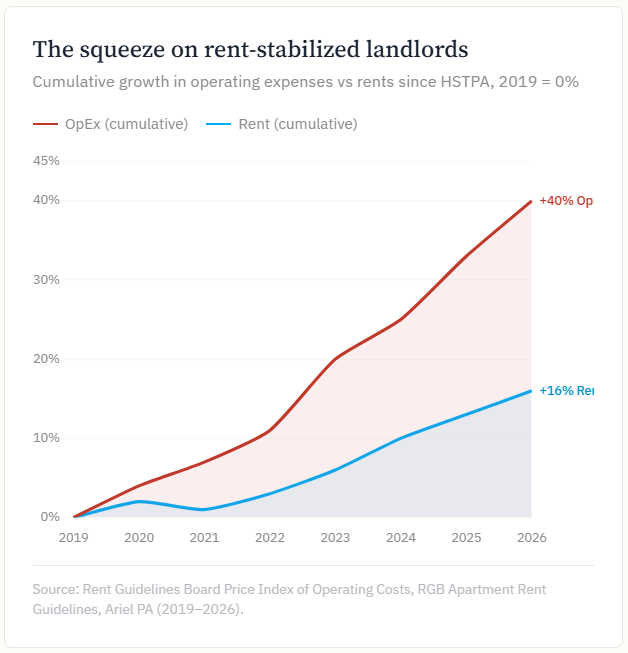

The most important valuation pressure is net operating income. In Q1 2026, Ariel reported that cumulative operating expenses had grown 40% since 2019, while rent growth had increased only 16%, creating a 24-percentage-point gap. That is the assessment issue in its simplest form: if regulated income cannot keep pace with expenses, NOI compresses. If NOI compresses, market value should decline.

Source: New York City Q1 2026 Multifamily Quarter in Review · Ariel Property Advisors

For property tax assessment purposes, this distinction is critical. Debt service is not treated as an operating expense in the assessment model, but rising interest rates still affect value because they affect capitalization rates, refinancing risk, and buyer demand. DOF defines operating expenses as property operating costs, excluding mortgage principal and interest and excluding property taxes for assessment purposes.

The capital markets have made the problem worse. Many rent-stabilized buildings were financed or refinanced when rates were lower. As those loans mature or reset, owners may face cash-in refinancings or out-of-pocket capital requirements. Ariel also notes that traditional lenders to rent-stabilized multifamily have retreated from the market, leaving owners with fewer refinancing options and forcing more portfolios toward distress.

That should matter when reviewing a Notice of Property Value. If DOF’s model assumes income, expenses, or capitalization rates that do not reflect the current economics of heavily rent-stabilized buildings, the resulting market value may be overstated. A rent-stabilized building with capped revenue, rising insurance, Local Law 97 exposure, repair obligations, collection issues, and limited financing availability should not be valued as if it were a conventional growth asset.

Transaction data reinforces the point, but only because it shows distressed pricing. In 2025, predominantly rent-stabilized assets represented 41% of transactions among larger multifamily and mixed-use buildings, but only 18% of dollar volume. Ariel described the pattern as evidence of “deepening distress and forced transaction activity.” That is not strong demand; it is the market clearing at lower prices.

The same pattern continued into 2026. Ariel reported that Q1 2026 rent-stabilized dollar volume appeared strong on the surface, but was largely driven by one distressed trade: the Pinnacle Group’s 5,100-unit portfolio, which entered Chapter 11 and was acquired for $451.3 million. Excluding that outlier, rent-stabilized volume would have been materially lower and more consistent with recent quarters.

For owners, the assessment should be tested against the property’s actual economics.

A proper review should compare the NOPV’s estimated income, expenses, and capitalization rate against the building’s actual rent roll, regulatory status, vacancy, arrears, insurance costs, repairs, and compliance costs. RPIE filings are especially important because DOF uses income and expense information each year to value income-producing properties.

Owners should also remember that a DOF Request for Review is not the same thing as a Tax Commission appeal. DOF states that owners who disagree with the assessed value on the NOPV may appeal to the New York City Tax Commission, which can reduce assessed value, change tax class, and adjust exemptions. DOF also notes that where an “effective market value” applies, the owner must prove that the current market value is lower than the effective market value to prevail.

The broader point is this: rent-stabilized multifamily buildings have been repriced by the market. The assessment system should not ignore that repricing. A building whose market value has declined because rents are capped, expenses are rising, capital is scarce, and buyers require a higher return should not be assessed as though the pre-HSTPA valuation model still applies.

For many rent-stabilized owners, the property tax appeal is no longer just about shaving a few dollars off the tax bill. It is about forcing the assessment to reflect economic reality.

This blog is a form of attorney advertising. We provide this information as a service to our clients and other readers for educational purposes only. Nothing in this blog should be construed as, or relied upon, as legal advice or as creating a lawyer-client relationship.