NYC Property Tax

Proposed Property Tax Abatement to Incentivize Fast Facade Repairs and Penalize Lingering Sidewalk Sheds

Published 4/21/2026 at 8:38 AM

By: Benjamin M. Williams

New York City building owners may soon have a new reason to finish facade work quickly and remove sidewalk sheds promptly. Senate Bill S9959, introduced by Senator Erik Bottcher on April 17, 2026, would create the RESTORE Act – the Reducing Excess Scaffolding and Timely Ongoing Repair Efforts Act. As of April 21, 2026, the bill is active and pending in the Senate Cities 1 Committee.

The bill would do two things at once. First, it would create a one-year property tax abatement for eligible owners who complete qualifying exterior-wall repairs and remove the related sidewalk sheds within 12 months. Second, it would impose property tax penalties where covered repairs and related shed removal take more than 18 months.

For owners deciding between this proposed benefit and J-51 Reform (J-51-R), the practical assumption should be that both benefits cannot be claimed for the same or similar facade work. J-51-R contains anti-duplication rules that prohibit a concurrent abatement or exemption for rehabilitation or new construction under another state or local law, and that also bar J-51-R for the same or similar item of eligible construction where another exemption or abatement is already being received as of the relevant December 31.

What buildings would be eligible for RESTORE?

RESTORE is drafted for a city with a population of one million or more, so it is aimed at New York City. The bill is not limited to residential buildings, Class 2 property, rent-regulated buildings, affordable housing, cooperatives, or condominiums. Instead, eligibility turns on whether the building is making or has made “covered repairs.”

| RESTORE term | Meaning |

|---|---|

| Covered building | A building that is making or has made covered repairs. |

| Covered repairs | Repairs to the exterior walls of a building that are either required after notification to DOB of an unsafe condition under NYC Administrative Code § 28-302.5, or made to prevent an unsafe condition. |

| Sidewalk shed requirement | The exterior-wall work must require a sidewalk shed because of the building’s height and the nature of the repairs, under Building Code § 3307.6.2(3). |

| Covered building owner | The owner of a covered building, including a private landlord, cooperative housing corporation, or condominium association. |

Although the bill’s legislative findings focus on Local Law 11/FISP buildings over six stories, the operative eligibility language is the covered-repair definition. In practice, the bill is designed for facade-safety work that requires a sidewalk shed and either corrects an unsafe condition or prevents one.

What tax benefit would RESTORE provide?

A covered building owner would be eligible for the abatement only if the owner completes the covered repairs and removes all sidewalk sheds installed in connection with those repairs within 12 months after the sheds were installed. The abatement would be available in the tax year in which the repairs are completed and the associated sheds are removed.

The abatement would be calculated as:

Abatement percentage x the lesser of (1) the cost of covered repairs or (2) the property taxes associated with the covered building for the completion tax year.

That makes RESTORE a potentially valuable but tightly timed one-year benefit. It is not a multi-year abatement, and it is capped by the lower of project cost or one year’s property taxes.

| Timing from shed installation to completion/removal | RESTORE abatement calculation percentage |

|---|---|

| Within 3 months | 50% |

| 4 months | 45% |

| 5 months | 40% |

| 6 months | 35% |

| 7 months | 30% |

| 8 months | 25% |

| 9 months | 20% |

| 10 months | 15% |

| 11 months | 10% |

| 12 months | 5% |

| More than 12 months | No abatement |

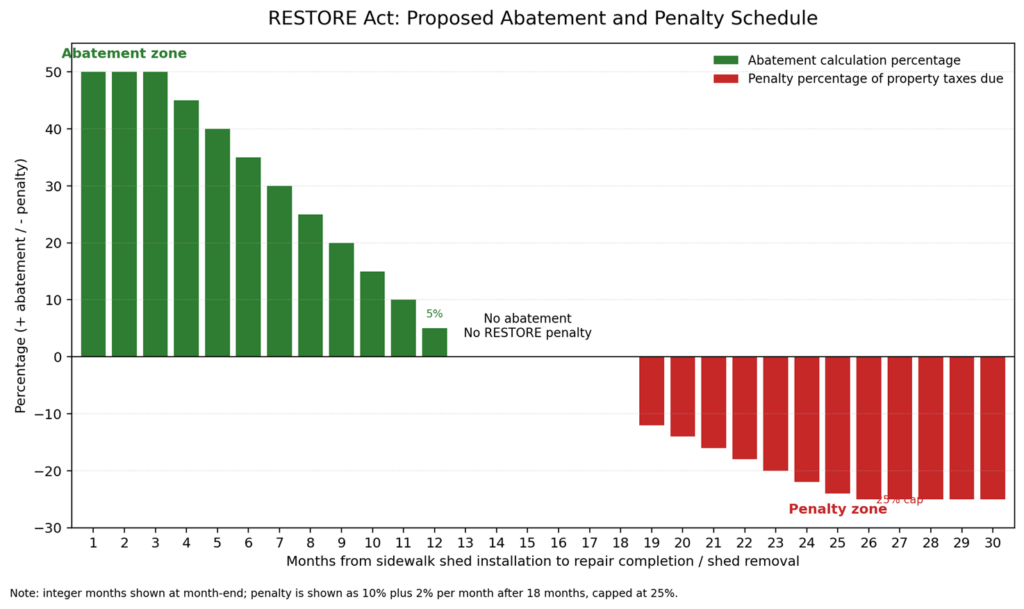

The RESTORE schedule in one chart

The chart below shows the proposed RESTORE abatement percentages as positive values and the proposed penalties as negative values. Green bars are abatements; red bars are penalties.

Figure 1. Proposed RESTORE Act abatement and penalty schedule. Percentages are not dollars; the abatement percentage applies to the lesser of covered repair cost or completion-year property taxes, while the penalty percentage applies to property taxes otherwise due.

What happens after 12 months and after 18 months?

RESTORE has two separate timing cutoffs. After 12 months, the abatement disappears. After 18 months, the penalty begins.

| Timing | RESTORE consequence |

|---|---|

| 0–12 months | Potential abatement, declining after month 3. |

| More than 12 months through 18 months | No abatement, but no RESTORE penalty yet. |

| More than 18 months | Penalty applies until the covered repairs are completed and the related sheds are removed. |

The proposed penalty equals 10% of property taxes otherwise due, plus 2% for each additional month after 18 months that the sidewalk sheds remain installed. The penalty is capped at 25% of property taxes otherwise due in any tax year. The chart uses a month-end view, so the first full month after month 18 is shown as the base 10% plus one 2% increment.

What would owners need to do to qualify?

The bill would require the owner to submit proof of timely compliance to the New York City Department of Finance. DOB would provide DOF with information needed to administer the program, and DOF would issue rules. Until those rules are adopted, owners should assume they will need a clean record of the shed installation date, repair scope, unsafe-condition or preventive-repair basis, shed removal date, completion date, covered repair cost, and tax bill.

| Documentation item | Why it matters |

|---|---|

| Sidewalk shed installation date | Starts the RESTORE clock. |

| Description of exterior-wall work | Shows the work is covered repair work. |

| Unsafe-condition notice or preventive-repair rationale | Shows the work fits the statutory definition. |

| Basis for sidewalk shed requirement | Shows the shed was required because of building height and repair type. |

| Repair completion date | Determines abatement eligibility and percentage. |

| Sidewalk shed removal date | Also required to stop the clock and determine eligibility. |

| Covered repair cost | Used in the abatement formula. |

| Property taxes for completion tax year | Used in the abatement cap. |

For ongoing projects, the abatement clock would use the original sidewalk shed installation date, even if that date predates the law’s effective date. The penalty transition rules are more forgiving: if repairs have been underway for less than one year when the law takes effect, prior time does not count toward penalties; if they have been underway for more than one year, time beyond the first year may count, but no project would be penalized if the repairs are completed and sheds are removed within six months after the effective date.

Owners could dispute penalties before DOF. DOF could waive or reduce a penalty if the owner shows that delay resulted from factors outside the control of both the owner and the entities hired by the owner. However, the scale and scope of the repairs would not count as factors outside the owner’s control. A dissatisfied owner could appeal DOF’s penalty decision to the New York City Tax Commission within 30 days.

RESTORE versus J-51-R: assume it is an election for the same work

For buildings that can qualify for both programs, the key question is not simply “Which one has the higher stated percentage?” The better choice depends on the property type, the eligible work, HPD’s certified reasonable cost, annual property taxes, timing, rent-regulatory consequences, and present value.

J-51-R is narrower than RESTORE. HPD describes J-51-R as an as-of-right real property tax abatement for certain residential rehabilitation of Class A multiple dwellings. Eligible construction must be on HPD’s certified reasonable cost schedule, meet a $1,500-per-dwelling-unit minimum scope threshold, have a completion date after June 29, 2022 and before June 30, 2026 (unless the law is extended), be completed not more than 30 months after commencement, and not be attributable to increased cubic content.

J-51-R benefits can be larger in total dollars: up to 8 1/3% of the total certified reasonable cost each year for up to 20 years, capped at 70% of approved certified reasonable costs. But J-51-R is not based on actual cost alone. It is based on HPD-certified reasonable cost, and it carries eligibility and compliance conditions that RESTORE does not.

| Issue | RESTORE | J-51-R |

|---|---|---|

| Status | Proposed; not enacted. | Existing program, subject to current deadlines. |

| Eligible buildings | Covered buildings in NYC making qualifying exterior-wall repairs requiring a sidewalk shed. | Eligible Class A multiple dwellings, including qualifying affordable rental, low assessed value cooperative & condominium, and regulated homeownership buildings. |

| Work focus | Exterior-wall repairs tied to unsafe conditions or preventive facade work requiring a sidewalk shed. | Eligible residential rehabilitation items on HPD’s certified reasonable cost schedule. |

| Benefit amount | Up to 50% of the lesser of covered repair cost or one year’s property taxes. | Up to 70% of HPD-certified reasonable cost, paid over time. |

| Duration | One tax year. | Up to 20 years. |

| Timing pressure | Complete repairs and remove sheds within 12 months for any abatement; penalty after 18 months. | Complete within program window and within 30 months after commencement; application and pre-commencement rules also apply. |

| Rent consequences | No rent-regulatory quid pro quo appears in the bill text. | Rental buildings may face rent-stabilization restrictions and must waive MCI rent increases attributable to eligible construction receiving benefits. |

| Duplication issue | Should be treated as unavailable for the same work if J-51-R is claimed. | Anti-duplication rules bar concurrent or same/similar item benefits, subject to statutory exceptions. |

Rule of thumb: when is each benefit better?

Use this simplified comparison:

RESTORE ~= RESTORE percentage x min(actual covered repair cost, completion-year taxes)

J-51-R ~= 70% x HPD-certified reasonable cost, paid over multiple years

If the RESTORE tax cap is not binding, J-51-R wins in nominal dollars when 70% of certified reasonable cost exceeds the RESTORE percentage times actual covered repair cost. At the maximum RESTORE rate, that means J-51-R nominally wins only if HPD-certified reasonable cost is more than about 71.4% of actual covered repair cost.

| RESTORE timing | RESTORE percentage | J-51-R nominal break-even if annual taxes are high enough |

|---|---|---|

| Within 3 months | 50% | J-51-R wins if certified reasonable cost exceeds 71.4% of actual cost. |

| 4 months | 45% | J-51-R wins if certified reasonable cost exceeds 64.3% of actual cost. |

| 6 months | 35% | J-51-R wins if certified reasonable cost exceeds 50.0% of actual cost. |

| 9 months | 20% | J-51-R wins if certified reasonable cost exceeds 28.6% of actual cost. |

| 12 months | 5% | J-51-R wins if certified reasonable cost exceeds 7.1% of actual cost. |

This is only a nominal-dollar rule. RESTORE is a one-year benefit, while J-51-R is paid over time. A present-value analysis can make RESTORE more attractive, especially where the project is completed quickly and the building’s annual taxes are large enough to absorb the RESTORE benefit.

Practical examples

Example 1 – J-51-R likely wins. A building spends $1,000,000 on eligible facade work, the RESTORE tax cap is not binding, and HPD-certified reasonable cost is also $1,000,000. If the owner completes the work and removes the shed within three months, RESTORE would be worth $500,000. J-51-R would be worth up to $700,000 over time. On nominal dollars, J-51-R wins.

Example 2 – RESTORE likely wins. The same building spends $1,000,000, but HPD-certified reasonable cost is only $500,000. RESTORE at the maximum rate would be worth $500,000. J-51-R would be worth up to $350,000 over time. RESTORE wins before even accounting for present value or J-51-R compliance costs.

Example 3 – J-51-R likely wins because of RESTORE’s tax cap. The facade project costs $1,000,000, but the building’s property taxes for the RESTORE completion year are only $300,000. At the maximum RESTORE rate, the benefit would be only $150,000. If J-51-R certified reasonable cost is $1,000,000, J-51-R could be worth up to $700,000 over time.

Bottom line

RESTORE would reward speed. J-51-R rewards qualifying residential rehabilitation. If a building is eligible for both and the owner cannot claim both for the same or similar facade work, the owner should model both before filing.

RESTORE is likely better where the project can be completed and the shed removed very quickly, the building has enough tax liability to absorb the one-year benefit, HPD’s certified reasonable cost would be materially below actual cost, or J-51-R’s rent-regulatory and MCI-waiver consequences are too costly.

J-51-R is likely better where the building qualifies cleanly, the certified reasonable cost is close to actual cost, the owner can use a multi-year benefit, the RESTORE tax cap is limiting, or the work will not be completed quickly enough to earn a meaningful RESTORE percentage.

Either way, owners should preserve both options at the planning stage: track RESTORE shed and completion dates, and, if J-51-R is a possibility, satisfy J-51-R pre-commencement and tenant-notice requirements before work starts. The worst outcome would be missing J-51-R procedural requirements, losing RESTORE because the shed stayed up too long, and still being exposed to RESTORE penalties after 18 months.

This post is for general informational purposes only. It is not legal advice, and readers cannot use it as legal advice. Whether a particular property should use RESTORE or J-51-R depends on the property’s actual facts, documents, and applicable law.