NYC Property Tax

Proposed Albany Bill Would Let NYC Choose a Lower Class Share Cap for FY 2026

Published 5/28/2025 at 9:00 AM

By: Benjamin M. Williams

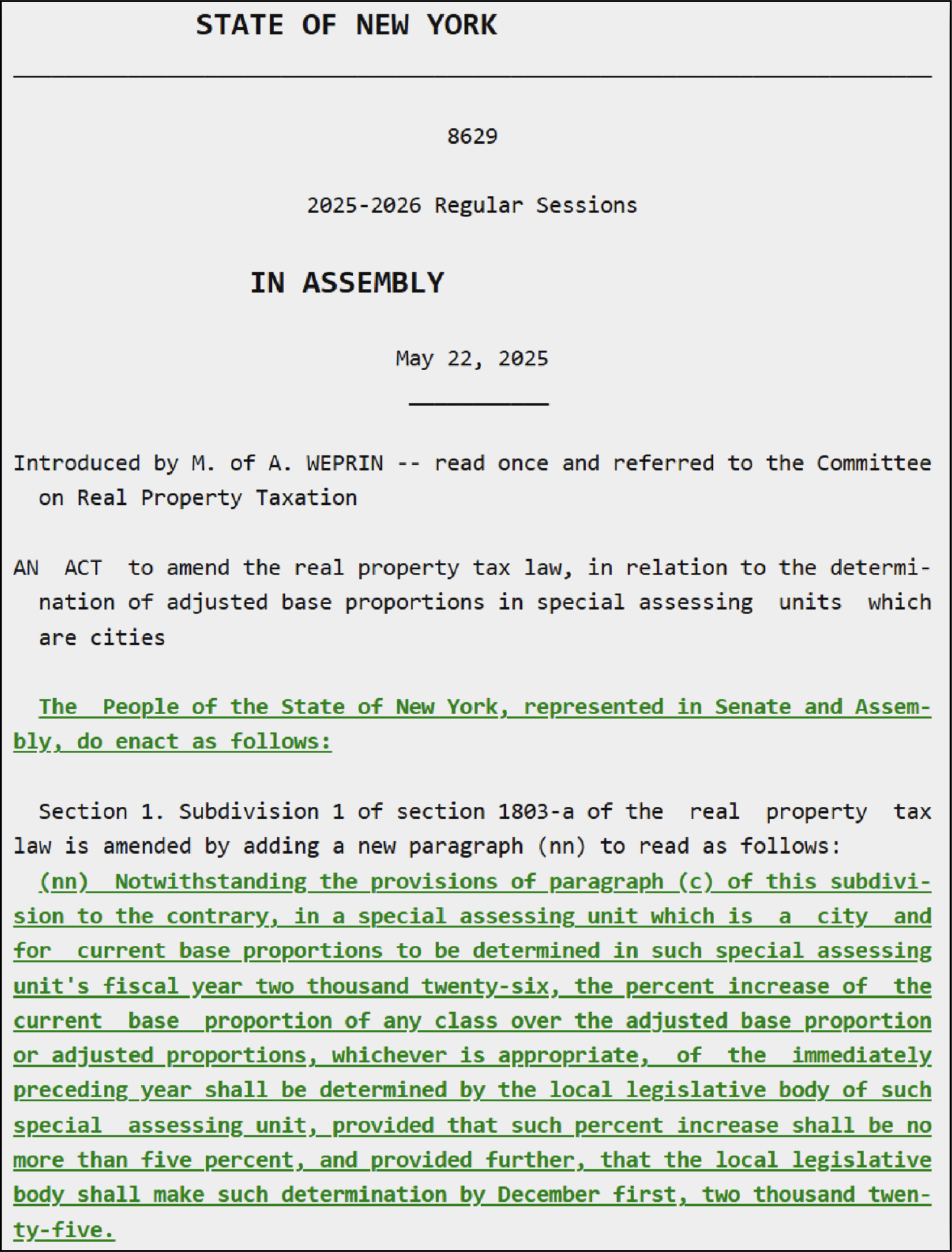

New legislation, Assembly Bill A8629 and Senate Bill S7980, introduced on May 22, 2025, would provide New York City with continued flexibility in managing property tax distribution among its four classes for fiscal year 2026. Specifically, this bill proposes adding a new paragraph (nn) into Real Property Tax Law § 1803-a(1), allowing the city to set an annual cap on the growth of each tax class’s share of the total levy anywhere from 0% up to the existing maximum of 5%. This approach mirrors prior legislative actions taken for fiscal years 2021, 2023, 2024, and 2025, aimed at reducing sudden tax burdens primarily on class 1 properties, which consist of one- to three-family homes.

The rationale behind this flexibility is that equalization rates, which are recalculated each October based on market valuations, have historically caused disproportionate increases in the tax levy for class 1 properties. Without intervention, these increases could lead to significant financial strain for homeowners. This bill would allow the City Council to adopt lower annual growth caps, thereby smoothing out potentially abrupt shifts in tax burdens across different classes.

Should the bill pass, the City Council must decide the specific cap by December 1, 2025. If enacted after initial fiscal year 2026 bills have already been issued, the bill contains provisions authorizing the Department of Finance to issue amended tax bills and recalculated rates, ensuring compliance with the new cap.

Potential impacts of this legislation vary across property classes. Class 1 would likely see reduced tax increases compared to the default scenario, offering homeowners financial relief. Conversely, tax classes 2 (multifamily residential properties including rentals, co-ops, and condos), 3 (utility properties), and particularly class 4 (commercial properties), could face increased burdens as they compensate for lower growth in class 1’s share.

While this bill provides important relief and stability for homeowners, it continues a recurring annual legislative pattern rather than addressing longer-term reform of the property tax system. Annual renewals could increase uncertainty for property owners and investors trying to project future costs. Additionally, critics point out that this repeated approach potentially shifts tax burdens disproportionately onto commercial and rental properties, raising broader equity concerns.

In conclusion, Bill A8629/S7980 gives New York City important short-term fiscal management tools but underscores the ongoing need for comprehensive property tax reform to address underlying distributional and valuation challenges.