NYC Property Tax

Property Values and the Looming Crisis in New York City’s Property Tax Base

Published 9/9/2024 at 4:47 PM

By: Benjamin M. Williams

As property tax appeals grow and cities across the country face shrinking revenues due to declining commercial property values, the impact on New York City’s budget is becoming increasingly apparent. I was recently quoted in this Bisnow article discussing how cities are scrambling to find solutions to the budgetary shortfalls caused by the post-pandemic decline in office property values. In New York City, like many other cities, the shift to remote work has altered the commercial real estate landscape, resulting in rising vacancy rates and decreasing market values, particularly in Class B and C office buildings. These changes are creating financial challenges for local governments, but they also present unique opportunities to rethink our approach to property taxes.

The Impact of Declining Property Values on Tax Revenues

Office buildings account for 21% of New York City’s property tax base, contributing around $7 billion annually. The decline in office property values will place substantial pressure on property tax revenues, a key source of funding for local governments. The gradual fall in market values could have long-term consequences for the city’s budget, as commercial office properties represent a significant portion of the tax base.

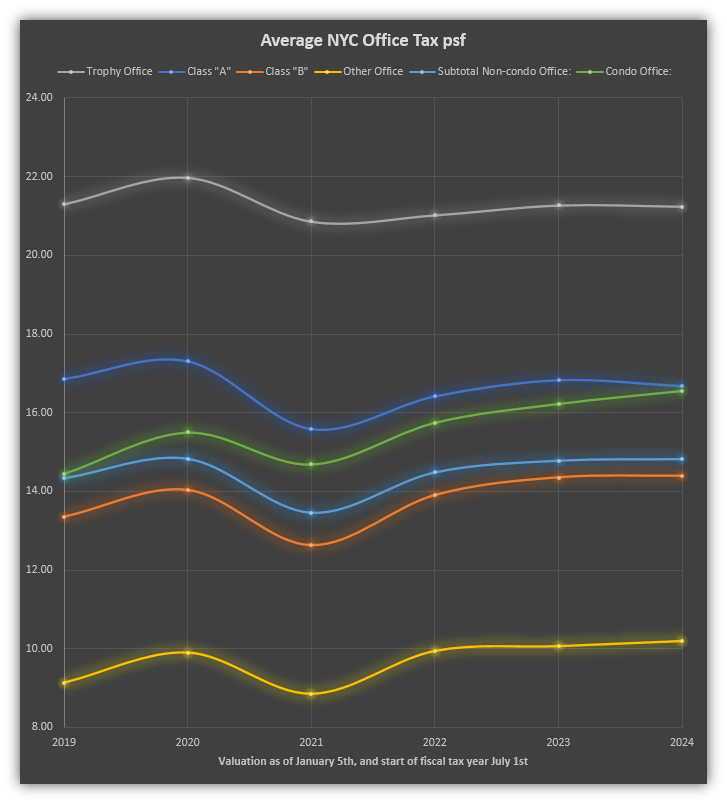

The recent Bisnow article highlighted the fact that cities like Boston, San Francisco, and New York are struggling to reconcile current tax revenues with the reality of declining property values. Office buildings are trading at significant discounts, yet property tax assessments remain high, creating tension between landlords and city officials. In New York City, despite declining market values, the Department of Finance has increased taxable assessed values for the 2025 fiscal year, with Trophy buildings seeing a 3.4% increase, Class-A properties rising 3.0%, and Class-B offices seeing a 2.6% bump. See my below chart and note the drop in 2021 due to COVID.

As I mentioned in the article, many property owners are now relying on property tax reductions to keep their businesses afloat, and the number of appeals is growing rapidly. For many property owners, the ability to obtain property tax cuts is now critical to the financial health of their investments.

Why Are Property Values and Assessments Diverging?

The divergence between property values and tax assessments stems from the lagging nature of New York City’s property tax assessment process. Property assessments are based on past leasing and revenue data, meaning that market conditions are often not reflected in assessments until much later. This creates significant challenges during periods of rapid market decline, such as the one we are experiencing now.

Two main factors are driving the decline in property values:

- Occupancy Declines: With the shift to remote work, office vacancies are at record highs, especially in lower-tier buildings. This drop in demand has driven down market values for many properties, as landlords struggle to lease their space.

- Rising Interest Rates: The increase in interest rates has also played a significant role in reducing property values. Higher interest rates lead to higher capitalization (cap) rates, which reduce the overall value of income-generating properties like office buildings. As borrowing costs rise, investors are willing to pay less for the same cash flows, driving property prices down further.

The Revival of the Tax Lien Sale

Adding further pressure to commercial properties, New York City recently revived the tax lien sale. This policy subjects commercial properties with property tax arrears that are more than one year past due to potential foreclosure via tax lien sales. Many office buildings, already struggling with high vacancies and declining values, may face foreclosure if they cannot meet their tax obligations in time. For property owners, this increases the urgency for obtaining property tax relief, making the appeals process even more critical.

What Does This Mean for New York City?

While New York City is partially shielded from the worst of the property value declines because of its diversified tax base, with commercial property taxes accounting for only 12% of its overall revenue, the ongoing drop in office property values still poses a significant risk. The Tax Policy Center projects that New York could face a budget shortfall of $3.8 billion to $5.3 billion by 2031 due to falling office values.

This scenario could trigger what some experts are calling a “doom loop,” where falling property values lead to lower tax revenues, forcing budget cuts, which in turn contribute to further economic decline. While New York City is not yet facing this worst-case scenario, the risk is real, particularly for older, less-competitive office properties.

Even though the immediate fiscal crisis may be delayed, the long-term outlook is more uncertain. Office vacancies remain high, and values continue to decline. As market conditions worsen, pressure will grow on city officials to reassess property values. Failure to do so may force difficult decisions about whether to raise taxes or cut services in the years ahead.

The Way Forward: Adapting to a New Reality

To stabilize its property tax base, New York City must explore new strategies. One potential solution is to accelerate office-to-residential conversions. Many older office buildings, particularly in lower demand, are ripe for conversion into residential units, which would help ease both the vacancy crisis and the city’s housing shortage. However, these conversions are expensive and complex, and they will not solve the problem overnight.

Additionally, New York City may need to reconsider its property tax assessment methodology to better reflect real-time market conditions. The current system, which relies on historical revenue data, is slow to adjust to market shifts. Adopting more flexible, real-time assessments could prevent the kind of misalignment we see now, where property owners face inflated valuations that do not reflect the true state of the market.

Conclusion

New York City must adapt to the post-pandemic reality of its commercial real estate market. With office values falling due to both rising vacancies and higher interest rates, the city’s property tax base is at risk of significant erosion. Policymakers must take action to ensure the tax system remains resilient and reflects market realities. Whether through revisions to the tax assessment process or incentivizing office-to-residential conversions like through 467-m, bold action is needed to protect the city’s fiscal future.

The revival of the tax lien sale adds urgency to this situation. Office buildings with arrears are now at risk of foreclosure, and property owners need relief as soon as possible. The current situation is a wake-up call for New York City and other urban centers. As the office market continues to evolve, so too must the way we assess and tax these properties. If the city fails to adapt, it could face years of fiscal instability. Now is the time for innovative solutions that address both the short-term and long-term challenges facing New York City’s property tax base.