NYC Property Tax

Step Closer to Revising 2024/25 Tax Rates

Published 8/1/2024 at 11:50 AM

By: Benjamin M. Williams

On July 25, 2024, New York State Governor Hochul signed into law Chapter 210 of 2024.

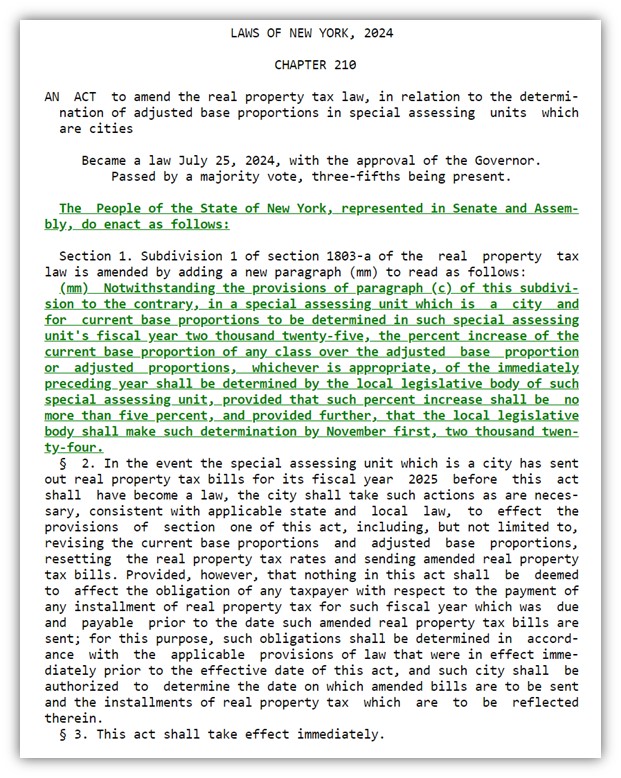

The new law amends the Real Property Tax Law, specifically section 1803-a, to allow the local legislative body of a “special assessing unit” (in this case, New York City) to adjust the “current base proportion” of property tax classes for the fiscal year ending 2025 (tax year 2024/25). This measure is intended to prevent disproportionate increases in tax liability for any single class of property owners, particularly focusing on residential properties.

The law on its own doesn’t do anything. It’s an enabling law. The law grants the City Council the authority to modify the percentage increase of the tax burden on any class, ensuring it does not exceed 5%, and requires this determination to be made by November 1, 2024. This allows the City Council to change the property tax rates that they already set for tax year 2024/25 but haven’t even used. See our prior post about the budget passing on June 30th and the City Council setting the “draft” rates: NYC Budget 2024/2025 and Property Tax Updates | Rosenberg & Estis, P.C. (rosenbergestis.com)

What’s the point of this law?

Without lowering the class share shift, more property tax burden gets shifted to tax class 1 (one- to three-family homes). As we previously advised, the tax class 1 property tax rate would have increased +4.1% or 81.4 basis points. Combined with the taxable assessed value increases, homeowners would have seen tax increases of +8.9% this year.

By reducing the tax burden on tax class 1, the tax burden must get shifted to the other tax classes. We expect the tax rates to increase for the other tax classes 2, 3, and 4.

What’s next?

The City Council is likely to vote and approve new tax rates, as they do every year as part of this base proportion adjustment process. We don’t yet know what these revised tax rates will be.

The City Council currently does not have a hearing scheduled to review the new tax rates but could do so as early as their next stated meeting on August 15th. The Committee of Finance typically reviews the matter first (their meeting is at 10:00 AM), and then it goes to the full City Council (their meeting is at 1:30 PM).

The NYC Department of Finance (DOF) already sent out tax bills on June 1, 2024, for the first half and quarter of tax year 2024/25 for payment due July 1, 2024. DOF calculated 2024/25 taxes due using last year’s tax rates from tax year 2023/24. Since DOF sent out the 2024/25 bills before this new law was enacted, DOF must revise those bills to reflect the new rates. DOF will likely do this on the November 2024 bills for payment due for the second half and third quarter (January 1, 2025) and fourth quarter (April 1, 2025) of tax year 2024/25. It’s a “make up” rate. If DOF billed at 12.5% for the first half, and the revised rate is 12.4%, then they essentially bill 12.3% for the second half to make the total tax year effective rate 12.4%.

Justification

Senator Andrew Gounardes sponsored the bill, and his justification was:

State law requires New York City to set class shares based on rates calculated by the State Board of Real Property Services (SBRPS) to distribute the tax levy among the four property classes. In most years, the State Board’s class equalization rates increase the tax burden on Class 1 properties, which include one-, two-, and three-family homes.

Currently, state law stipulates that the current base proportion of any class cannot exceed the adjusted base proportion of that class from the previous year by more than five percent. This bill allows the local legislative body to reduce the cap on the maximum growth rate of any tax class’s share of the overall tax levy. The flexibility to lower this cap enables the Council to set fiscal [2025] tax rates that provide relief to residential properties in Class 1 without imposing excessive burdens on other property classes.

Without this legislation, the New York City Council would be required to adopt the default SBRPS formula for class shares, potentially resulting in unfair tax rates for certain property classes. This bill gives the City Council the flexibility to set property tax rates that prevent any single group of property owners from experiencing a significant spike in tax liability compared to the previous year.

Streamlining the process

The bill passed both houses by June 4, 2024, 26 days before the New York City budget was finalized. If it had been delivered to the Governor and she had signed it much sooner, then the City Council could have approved the final rates as part of the budget making process before June 30th. They would have saved the City Council some extra work. But DOF would still have had to send out bills with revised rates later in the year.

Every year the State seems to pass this enabling legislation. Then the City Council revises the rates. Rather than the state law being one-year fixes annually, the state should consider making it a permanent change, giving the City more local control over its property tax rates. This would cut down on the amount of legislation and work it takes to set tax rates every year.

Will we ever see a year where the legislators set the tax rates before DOF sends out the June tax bills, and the rates aren’t later changed?