NYC Property Tax

RPIE-2023 Non-Compliance – file by August 21, 2024

Published 7/29/2024 at 4:17 PM

By: Benjamin M. Williams

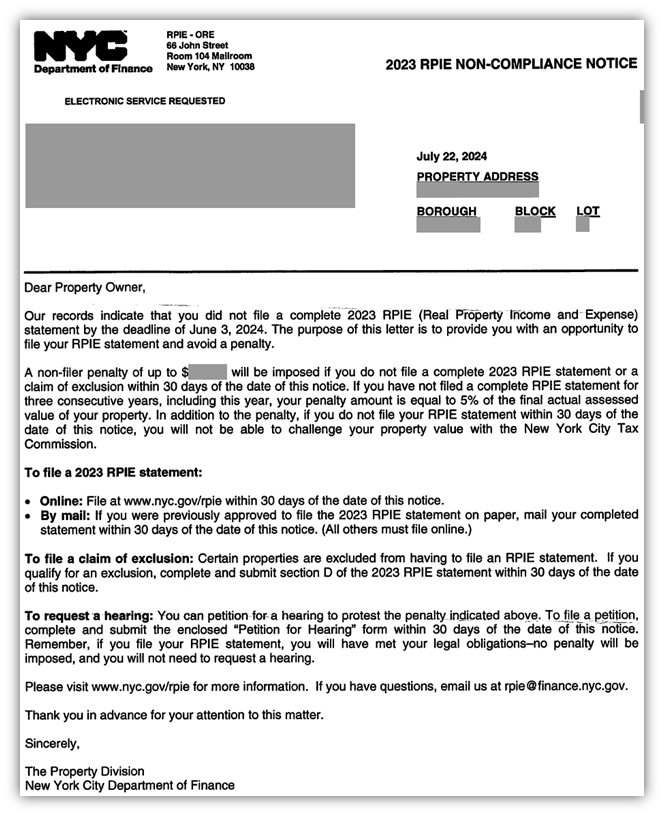

On July 22, 2024, the NYC Department of Finance (DOF) published the Real Property Income and Expense (RPIE) Non-Compliance list and mailed notices to owners. See the below sample Notice. This list consists of “income-producing” properties in New York City that the DOF has identified as of June 3, 2024, as having failed to submit a properly completed RPIE-2023 as required by City regulations.

Properties on the list have 30 days to file the RPIE-2023 to avoid the monetary penalties. The extended filing deadline is August 21, 2024. File online at http://nyc.gov/rpie on DOF’s SmartFile system.

Certain properties may be excluded from filing the RPIE-2023 and reporting income and expenses. Typical examples include properties that had no income in 2023 or were purchased in 2023. Nevertheless, these properties still have the affirmative duty to file the claim of exclusion on the RPIE-2023 form.

RPIE Non-Compliance Penalties

Owners that still don’t file by the extended filing deadline of August 21, 2024, will be subject to a fine. There are three types of fines.

- Owners who fail to file a claim of exclusion will be fined:

- $100 first year,

- $500 after the second consecutive year, or

- $1,000 for three or more years.

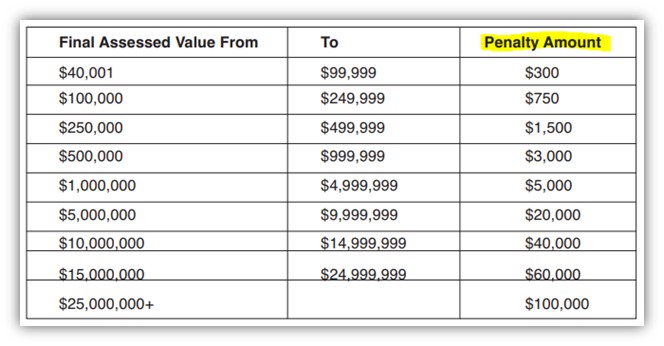

- Owners who fail to file for three consecutive years: 5% of the Assessed Value (AV).

- All other owners the penalty is based on where the 2024/25 Final Actual AV falls with the range of this table:

Read more here: property-rpie-non-compliance (nyc.gov) and rpiepenaltyinfo (nyc.gov)

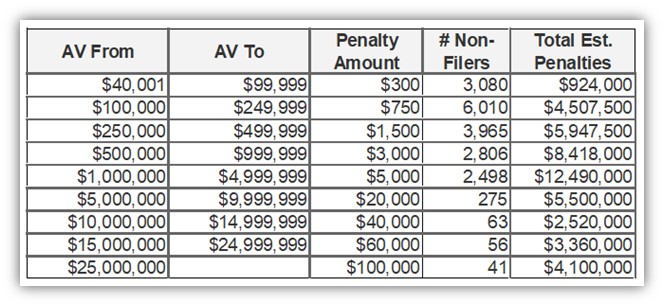

If hypothetically everyone on the RPIE-2023 list doesn’t file by August 21st and they are all subject to the penalty amounts in the table in #3 above, the total fines would be $47,767,000. Of course that won’t happen, as many people will end up filing or claiming an exclusion, or some will be subject to the 3-consecutive-years 5% penalty. See below by AV range for RPIE-2023:

You can see that almost half of all non-filers, 48.4%, have AVs less than $250,000. RPIE non-compliance is catching mostly small properties. 69.5% of all non-compliant properties have AVs less than $500,000, and 84.4% have AVs less than $1 million.

The $40,000 minimum AV threshold hasn’t changed in many years and isn’t tied to inflation increases. This minimum might be something legislators consider increasing to ease owners’ filing burdens and reduce the amount of non-compliant properties. Legislators might consider how useful the RPIE information really is for low AV properties, and if DOF does not use much RPIE data from properties with AVs less than $500,000, for example, then that could be a reasonable new threshold. Additionally, the legislators could have the RPIE minimum AV increased every five years to keep pace with general AV inflation, just like the TC309 form is. (The TC309 is the Tax Commission Accountant’s Certification of TC201 income and expenses for certain properties with AVs over $5 million, which threshold is subject to adjustments every five years.)

DOF budgeted $17.5 million in RPIE late penalties for fiscal year ending June 30, 2024. DOF budgets $12 million per year for subsequent years.

RPIE Non-Compliance History

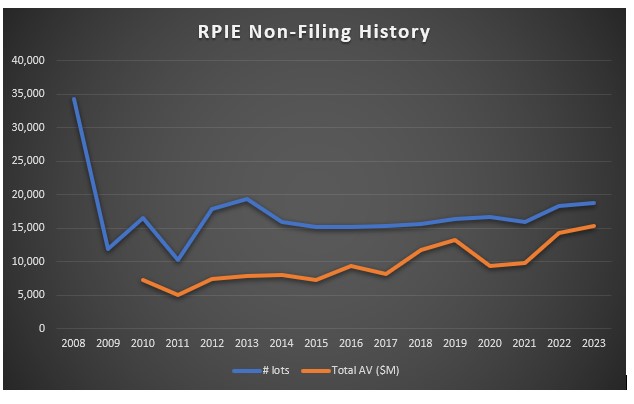

This year there are 18,794 properties on the RPIE-2023 non-compliance list, with total AV of $15.266 billion. That is the highest number of non-compliant properties in 10 years, and the highest AV in the 14 years that I have kept track.

RPIE-2023 Analysis

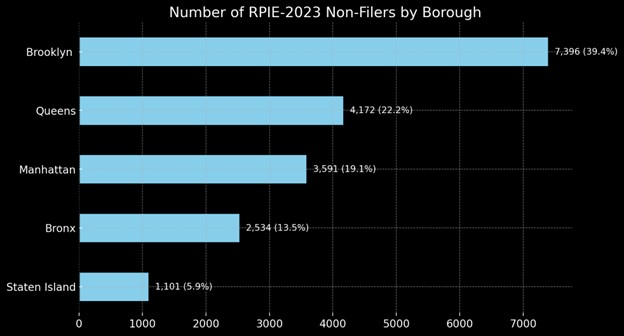

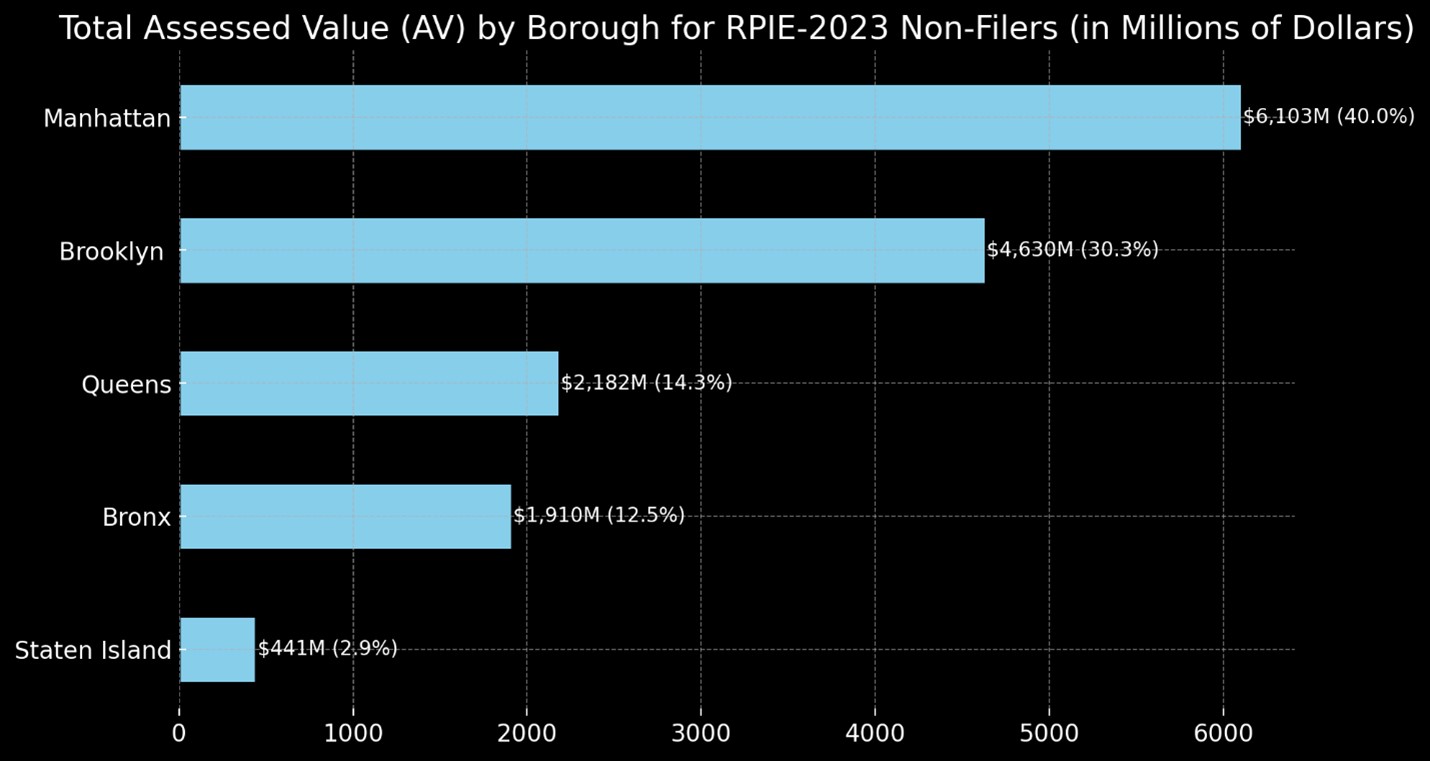

Brooklyn had the greatest number of non-filers, with 39.4% of all, and 30.3% of the total AV. Manhattan, which only had 19.1% of all non-filers, had 40.0% of the total AV.

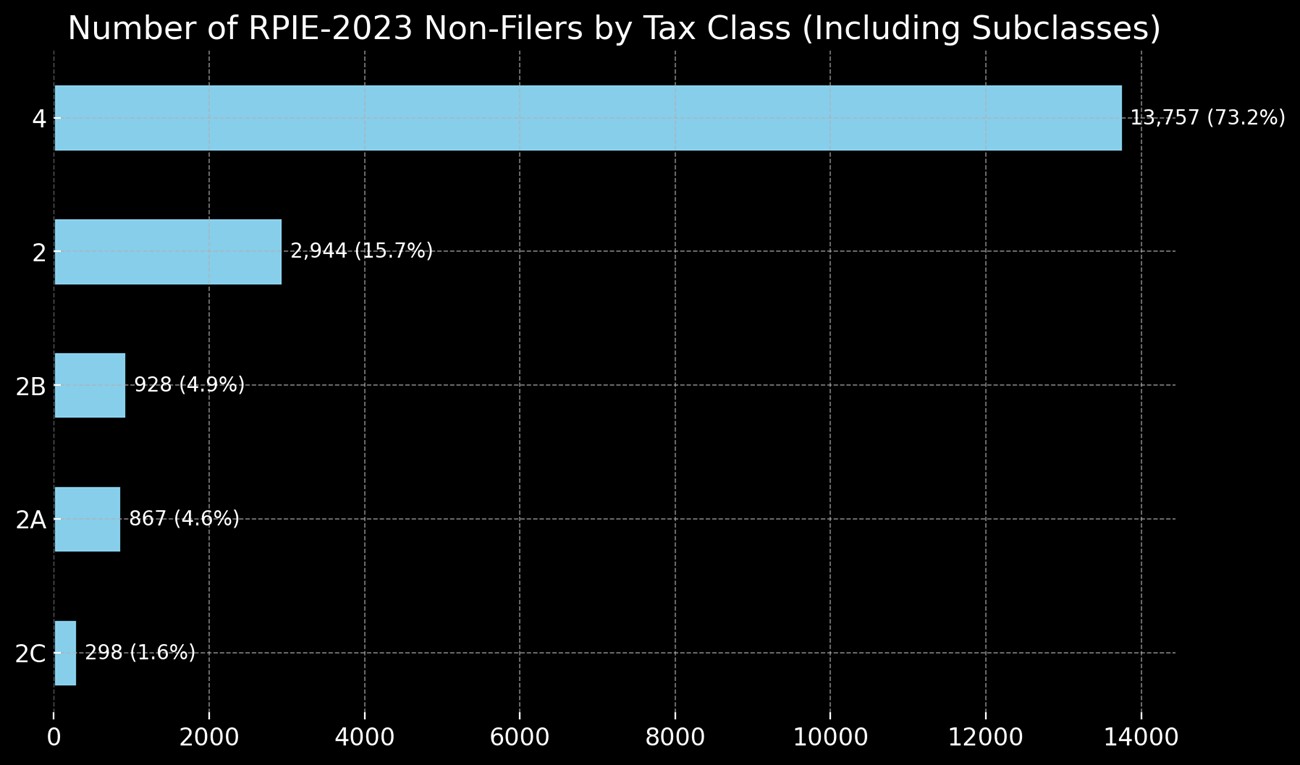

Tax class 4 (mostly commercial) had the greatest number of non-filers, with 73.2%:

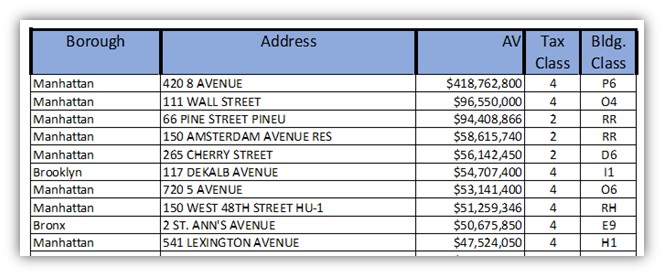

Only 41 properties had an AV over $25 million, the threshold for the $100,000 fine. Here are the top 10 largest by 2024/25

Actual AV:

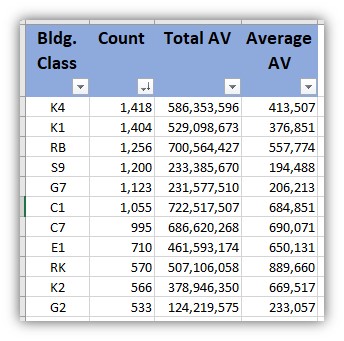

The most frequent Building Classifications were K4 and K1, both retail classifications, with average AV around $400,000. Followed by RB office condominiums. These are tax class 4. Here are the building classification counts over 500:

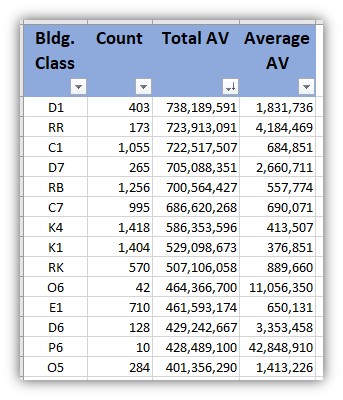

The greatest total AV was building classifications D1, RR, C1, and D7, which are all residential rental buildings (tax class 2). Here are the building classifications with Total AV over $400 million:

What is the RPIE?

The DOF uses income and expense information each year to value income-producing properties. Property owners provide this information by completing the RPIE statement. DOF uses the RPIE information to determine the property’s value for the following tax year.

The RPIE-2023 was due June 3, 2024. DOF will use this 2023 income and expense information to value properties for tax year 2025/26, with a taxable status and valuation date of January 5, 2025. DOF will publish the 2025/26 tentative assessment roll on January 15, 2025. These assessments will be used for taxes due July 1, 2025.

Who is required to file RPIE?

Owners of income-producing properties with an actual assessed value of more than $40,000 on the tentative assessment roll must file a Real Property Income and Expense statement or a claim of exclusion. For more information and to find out if you can claim an exclusion, review the RPIE filing information and frequently asked questions.