NYC Property Tax

NYC Property Tax Reform Legislation Proposed

Published 7/10/2024 at 11:05 AM

By: Benjamin M. Williams

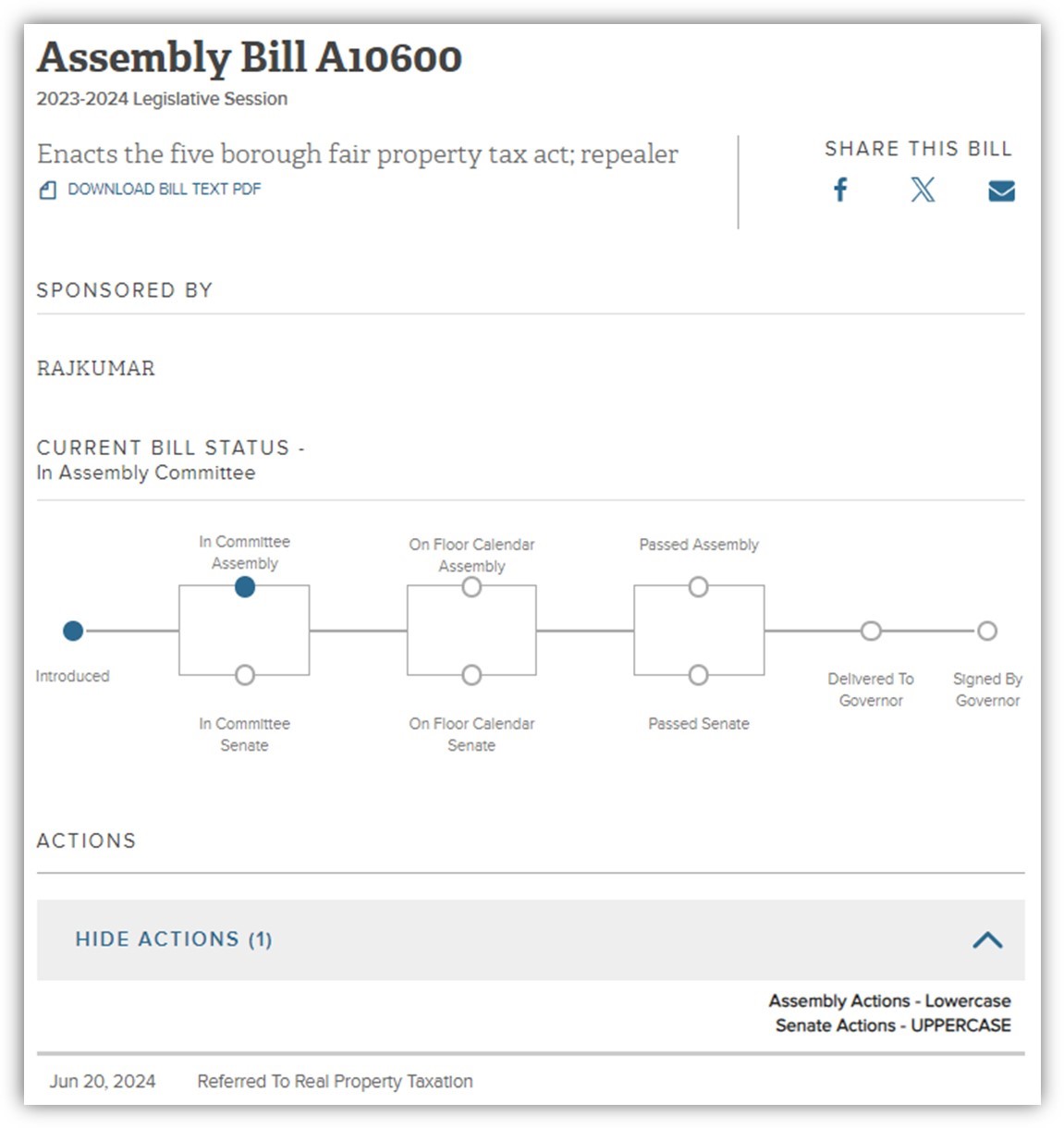

The Five Borough Fair Property Tax Act was introduced by the Committee on Rules Assemblymember Jenifer Rajkumar (Assembly District 38) as Assembly Bill A10600 on June 20, 2024. It was “read once” and referred to the state Assembly’s Real Property Taxation Committee, which doesn’t appear to have any upcoming meetings scheduled.

The proposed Five Borough Fair Property Tax Act will be the state legislature’s first attempt at reforming the NYC property tax system following the government’s recent loss in the Tax Equity Now NY LLC lawsuit, and the NYC Property Tax Reform Commission’s 10 recommendations to make the system more fair and transparent. It remains to be seen whether that is the case and who will be impacted by the proposed legislation, which we are following closely.

Why is this bill proposed? Here is the Justification paragraph taken directly from the bill memo:

“New York City’s arcane property tax system is rife with inequities. The use of assessed values with caps on growth results in assessments vastly below market value, resulting in artificially lower tax rates in gentrified neighborhoods. The coop-condo tax abatement also creates sweetheart tax rates for luxury buildings. Effective tax rates are now vastly different based on neighborhood, tending to be higher in low-income communities compared to those that gentrified. The Five Borough Fair Property Tax Act uses fair market value assessments, done by the NYC commissioner of finance, with a means-tested circuit breaker tax reduction to provide targeted relief to taxpayers who need it. The bill also repeals the coop-condo tax abatement, the overly complicated class share system, and the use of fractional assessments.”

The bill is structured into six parts A through F, which largely follow the Commission’s 10 recommendations (excerpted below):

- abolishing the class share system

- homestead exemption

- circuit breaker tax abatement

- assessment of residential cooperative, condominium and rental property

- cooperative housing corporations: and to repeal of a partial tax abatement for residential real property held in the cooperative or condominium form of ownership

- determination of fair market value

The New York State Assembly typically meets January to June, so this bill may not get legs until after the November 5, 2024, election. And I have not seen any indication that the New York City Council has weighed-in, or proposed any resolutions in favor or opposition, or scheduled any hearings on this proposed state legislation which would impact the city.

The New York City Advisory Commission on Property Tax Reform’s consensus on 10 final recommendations:

- Creating a new expanded residential class, consisting of 1-3 family homes, coops, condominiums, and 4–10-unit rental buildings. The property tax system would continue to consist of four classes of property: residential; large rentals; utilities; and commercial.

- Using a sales-based methodology to value all properties in the new residential class.

- Ending fractional assessments for all property types. Each property would be assessed at its full market value. This will result in an increase in the taxable base and the tax rate required to generate the same level of revenue will decrease.

- Eliminating current assessed value growth caps for the new residential class and instituting five-year transitional treatment for market value growth, whereby year-on-year changes in market values are phased-in over five years at 20 percent per year.

- Creating a partial homestead exemption for primary resident owners in the new residential class. This exemption should be either a flat rate or a graduated marginal rate exemption for primary resident owners with incomes up to $500,000, with a phase-out of the benefit for owners with incomes exceeding $375,000. The Commission recommends retaining all existing personal exemption programs and eliminating the current coop-condo abatement, since recommendations 1-4 negate the need for an abatement to address inequities between 1-3 family homes and coops and condos.

- Creating a circuit breaker, based on the ratio of property tax to income, in order to reduce the property tax burden on primary resident owners. The circuit breaker should be for primary resident owners with a ratio of tax paid to income exceeding 10 percent and incomes below $90,550, with the benefit phasing out for incomes exceeding $58,000. The benefit amount should be capped at $10,000.

- Eliminating the current class share system and replacing it with a system that freezes relative tax rates for five-year periods. Under the new system, while the Mayor and the City Council can adjust tax rates, the tax rates for all classes may only be altered on a proportional basis within each five-year period. There would no longer be changes in tax rates driven by market value shares, as under the current system. Every five years the city would conduct a mandated study to analyze whether adjustments are needed in order to maintain consistency in the share of taxes relative to the fair market value borne by each tax class.

- For properties not in the new residential class (rental buildings with more than 10 units, commercial parcels, and utilities), current valuation methods be maintained. There will be separate tax classes for rental buildings with more than 10 units, commercial parcels, and utilities. As noted in recommendation 3, the Commission recommends removing fractional assessments for all these tax classes.

- For the new residential class, phase-in to the new system should occur over five years. When a property transfers during the five-year transition period, it will be fully phased into the new system the fiscal year after the transfer.

- The City institute a mandatory comprehensive review of the property tax system every 10 years by the City.