NYC Property Tax

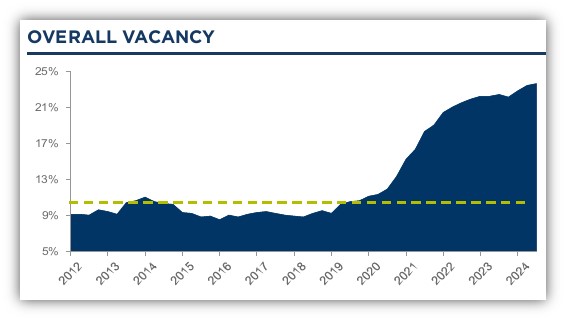

NYC office market vacancy status for Q2 2024

Published 7/19/2024 at 9:34 AM

By: Benjamin M. Williams

What are the real estate brokerages saying about the New York City office market in Q2 2024?

First, let’s look at the Office of the New York City Comptroller Brad Lander’s analysis: New York by the Numbers Monthly Economic and Fiscal Outlook No. 91 – July 9, 2024 (nyc.gov)

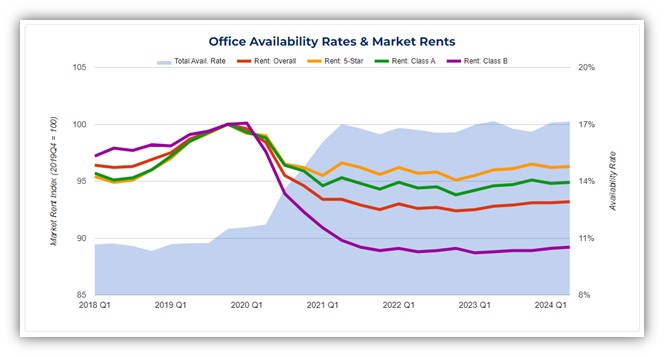

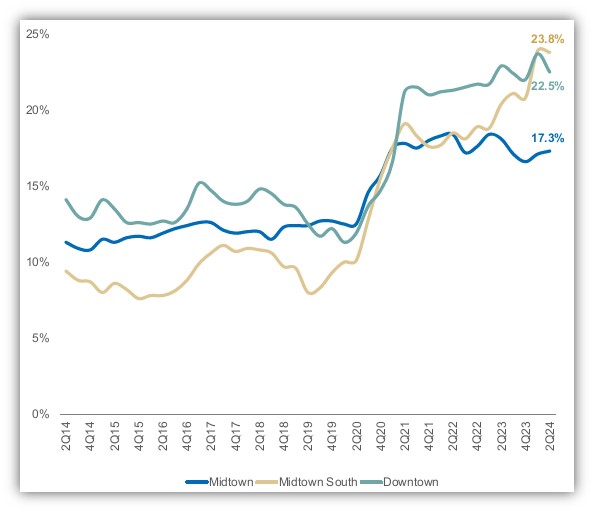

- New York City’s office market appears to have stabilized and even shown scattered signs of improvement, albeit from weak levels. Overall, office availability rates have held steady at around 17% citywide since the end of 2021, as shown in Chart 5 below.

- At the high end of the market, trends have been stronger: availability rates on 5-star (top tier) properties have retreated from elevated levels, despite a substantial volume of such space coming onto the market in just the past two years. In fact, since mid-2022, the amount of occupied 5-star office space has increased by more than 7 million SF or 14%, as virtually all of the new supply has been absorbed.

- Market asking rents, which had fallen about 7% citywide during the pandemic, have been virtually unchanged since the end of 2021. But this masks some crosscurrents within segments, as shown in Chart 5 below. Rents on 5-star (top-tier) space are down just 3-4%, whereas rents on Class B & C properties are down roughly 10%, though all segments of the market have seen steady rents for the past 2½ years. This general stability, combined with the relative strength at the high end of the market, strongly suggests that the potential “doom loop” scenario, in which commercial real estate tax revenues contract steeply causing a downward economic spiral, has not come to pass. as noted in our May Spotlight report.

- Chart 5:

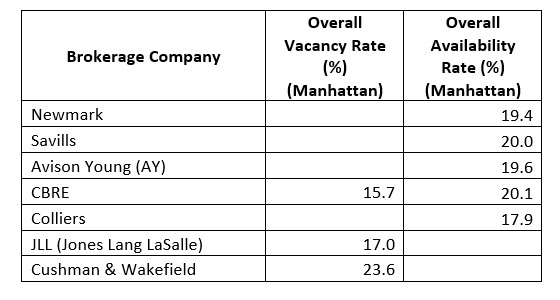

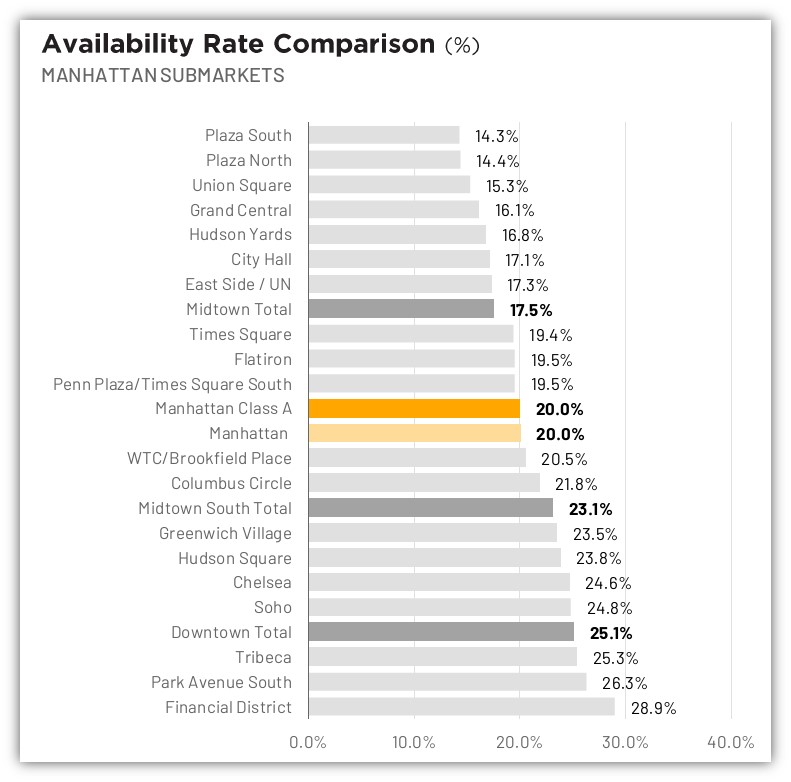

Source: CostarSummary of 7 (out of 8) brokerage companies vacancy/availability rates for Manhattan overallBut it really depends on the submarket (Midtown, Downtown, etc.) and class (Trophy, A, B/C)…

Cushman & Wakefield – Manhattan

(Source: Manhattan_Americas_Marketbeat_Office_q2-2024.pdf (cw-gbl-gws-prod.azureedge.net))Vacancy Rates and Availability:

- Overall Vacancy Rate: Edged up slightly by 20 basis points (bps) to 23.6%.

- Direct Vacant Supply: Reached a record high of 99.1 million square feet (msf).

- Sublease Space: Remained relatively stable at 22.6 msf, a slight decrease of 0.4% from a year ago.

Submarket Details:Midtown:

- Overall Vacancy: Increased modestly by 10 bps to 22.9%.

- Direct Vacant Space: Fell by 3.0% to 47.2 msf.

- Class A Vacancy: Decreased by 30 bps to 22.1%.

Midtown South:

- Overall Vacancy: Rose by 100 bps to 25.3%.

- Direct Vacant Space: Increased by 7.2% to 14.9 msf.

- Sublease Supply: Decreased by 8.4% to 3.3 msf.

Downtown:

- Overall Vacancy: Decreased by 10 bps to 24.6%.

- Class A Vacancy: Fell by 10 bps to 23.9%.

- Sublease Space: Increased slightly by 1.0% to 6.5 msf.

Overall Trends and Outlook:

- Despite an increase in leasing activity, the overall vacancy rate has slightly increased due to the high availability of direct vacant space.

- The absence of new construction completions and minimal space additions have influenced the vacancy dynamics.

- The market anticipates a strong leasing pipeline and potential new construction in the latter half of 2024, along with potential conversions or repositioning of older properties.

This report highlights the continued high vacancy rates in Manhattan’s office market, with substantial available direct and sublease spaces despite strong leasing activities. The trend indicates a slowly improving but still challenging office market environment.

Avison Young

(Source: Avison Young – Market Report)

Leasing Activity: Reached 14.6 million square feet (msf), an 18.7% increase from 2023, but still 30.7% below pre-COVID averages.

Availability Rate: Dropped slightly from 19.7% to 19.6%, with direct space decreasing by 700k sf and sublet space by 70k sf.

Class A Properties: Representing 15% of the market, they captured 42% of transaction activity, driven by large leases. This is the second-highest share in the past decade.

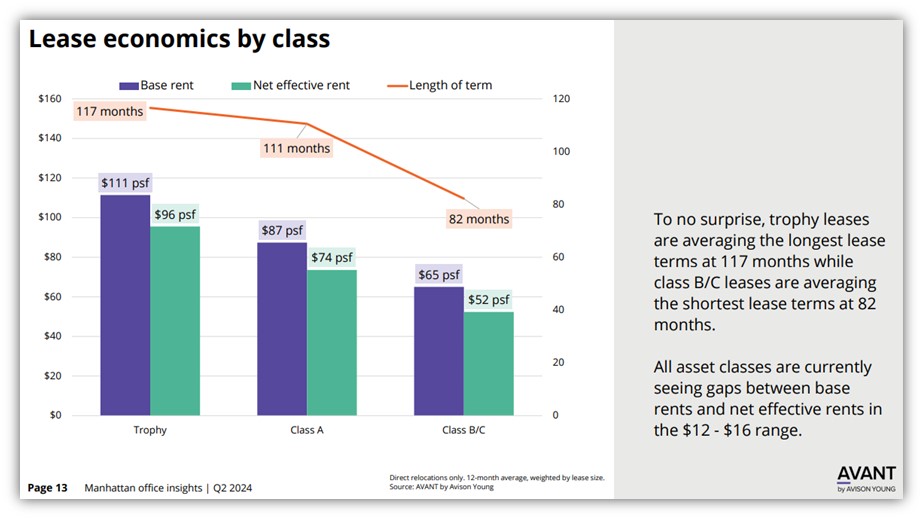

Tenant Improvement Allowances: Stabilized at $132 psf for both trophy and Class A properties, with 12 and 11 months of free rent, respectively.

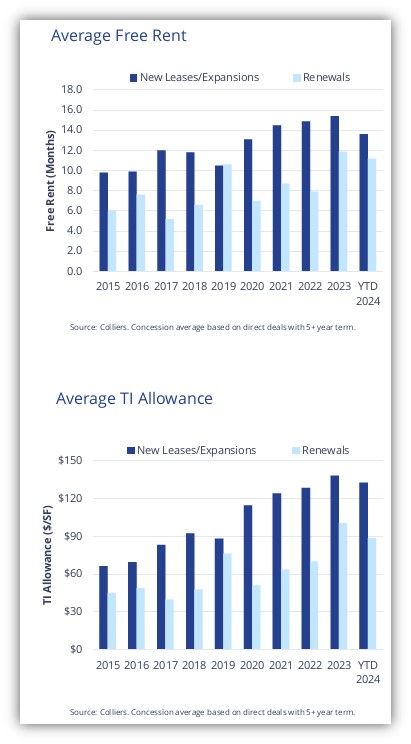

Colliers

(Source: NYC Q2 2024 Manhattan Office Report | Colliers)

The overall availability rate for Manhattan office space is 17.9%, a slight decrease from the previous quarter but a small increase from June 2023. The total available supply has grown by 79.5% since March 2020, reaching 96.66 million square feet. Sublet availability has also decreased by 0.25 million square feet in the quarter, yet sublet inventory is still 71.7% higher than in March 2020, totaling 20.44 million square feet. Large blocks of space over 250,000 square feet saw a decrease in the number of listings from 39 to 36 compared to Q1 2024, though this number is significantly higher than the 15 listings in Q1 2020.

Free Rent:

- The year-to-date weighted average rental abatement period for new deals and expansions in 2024 was 13.6 months, compared to 15.4 months for the full-year average in 2023.

- For renewals, the average abatement period was reduced to 11.2 months, compared to 11.9 months for the full-year average in 2023.

Tenant Improvement (TI) Allowances:

- The year-to-date average TI allowance for new deals and expansions in 2024 was $132.57 per square foot, which is 4.1% below the full-year 2023 average of $138.30 per square foot.

- For renewals, the year-to-date average TI allowance was $88.59 per square foot, an 11.8% decrease from the full-year 2023 average of $100.45 per square foot. However, this is still higher than the 2022 average of $70.09 per square foot

Overall Asking Rent:

- The average asking rent decreased for the fourth consecutive quarter by 0.3% during Q2. This decline was mainly due to below-average priced large blocks of space added to the available inventory, the leasing or withdrawal of above-average priced blocks of space, and instances of lower repricing across the market.

- The asking rent average was reduced by 1.5% year over year and was 6.6% below the March 2020 average.

Newmark

(Source: NYC Office Market Overview (nmrk.com))

Manhattan Overall Availability dropped by 10 basis points quarter-over-quarter to 19.4%. Free rent and work allowance deal concessions remain elevated but appear to be stabilizing.

Marcus & Millichap

(Source: New York City Office Market Report (marcusmillichap.com))

Vacancies:

- Manhattan: The report notes a decline in vacancy rates, particularly in Midtown Manhattan, where the local vacancy fell by 100 basis points year-over-year, despite increased office deliveries. The overall marketwide vacancy rate eased to 17.2%.

- Forecast: Despite notable space relinquishments in the first quarter, the metrowide vacancy rate is projected to end 2024 in line with the trailing three-year average of 17.1%.

Asking Rents:

Class A Spaces: The report indicates a sharper decline in asking rents for Class A spaces, which fell by 6.8% year-over-year, more than double the decline rate for Class B/C spaces.

Savills

(Source: Savills | Manhattan Q2 2024 Office Report)

JLL

(Source: New York Office Market Dynamics | Q2 2024 | JLL Research)

Vacancy Rates and Availability:

- Total Vacancy Rate: Stands at 17.0%, showing a downward trend.

- Sublease Space: Overall, sublease space availability decreased by 16% quarter-over-quarter.

- Class B Buildings: Despite a significant reduction in Class B inventory due to conversions, the Class B vacancy rate continues to trend upward, highlighting a persistent “flight-to-quality” trend where tenants prefer higher-quality spaces.

CBRE

(Source: Manhattan Office Figures Q2 2024 | CBRE)

The overall vacancy rate in Manhattan remained stable from the previous quarter at 15.7%, but this is up slightly from 15.6% a year ago.