Industry Updates

NYC Property Tax Rates for 2022/23

Published 6/15/2022 at 2:01 PM

By: Rosenberg & Estis, P.C.

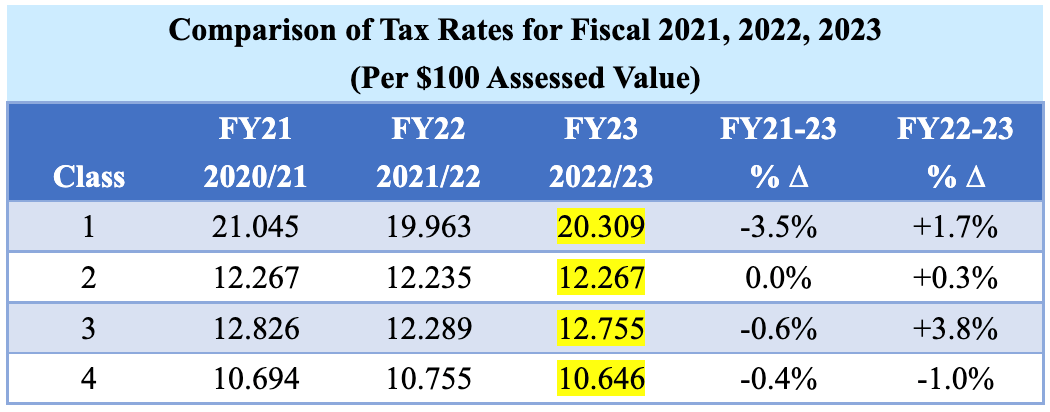

The New York City budget passed last night and the City Council set the fiscal year 2023 (7/1/2022 – 6/30/2023) property tax rates as follows:

The tax class 4 (commercial) tax rate had its first decrease in five years. The tax class 2 (apartment buildings) tax rate had its first increase in six years.

Tax year 2022/23 assessments saw large increases this year. Class 4 market values increased +9.73% from 2021/22, but are still -9.39% below pre-COVID 2020/21 because market values declined -17.42% from 2020/21 to 2021/22. Class 2 market values increased +9.05% this year, and are up +0.09% above pre-COVID 2020/21. The City’s taxable assessments increased +7.05% overall. When you combine changes in the taxable assessments and changes in the tax rates, tax class 2 taxes will increase +7.28% and tax class 4 +6.88% over last year.

Specific Manhattan market values increased as follows: tax class 2 rentals +7.1%, tax class 2 co-ops/condos +8.0%, class 4 offices +8.3%, and class 4 retail +10.3%. Brooklyn, Bronx, and Queens all had double-digit tax class 2 and 4 market value increases over 10%.

On June 4, 2022, the Department of Finance sent the tax bills for payment due July 1, 2022. You can view those bills online. DOF used the prior (Fiscal 2022) tax rate to compute the bills. DOF will use the new (Fiscal 2023) tax rates for the November 2022 bills which will be for payments due on or after 1/1/2023.

On June 2, 2022, the City Council established 0.5% as the tax year 2022/23 discount percentage for early payment of real estate taxes. That is the same rate since 2015. The Discount Rate is a tool to encourage prepayments.

On June 16, 2022, the City Council is scheduled to vote to establish the annual interest rates for the non-payment of property taxes for 2022/23. For 2021/22, the interest rates were as follows. For AVs > $450,000, the interest rate was 13% (down from 18%). For $250,000 < AV ≤ $450,000, the interest rate was 6% (down from 18%). For AVs ≤ $250,000, the interest rate was 3% (down from 3.25%-5%). For 2022/23, the Banking Commission recommended rates of 18% / 12% / 6%, but the City Council’s agenda indicates they will vote on rates of 14% / 7% / 4%. (The AV is the Actual Assessed Value; except for cooperative apartments where it is the AV per residential unit.)

DOF extended the RPIE-2021 filing deadline to June 5, 2022. The regular RPIE and Storefront Registry were due June 5. If you failed to file, you can still file now and avoid the monetary penalties. DOF extended the RPIE Rent Roll filing deadline to August 1, 2022. Class 2 and 4 property owners who have filed storefront information must file a Supplemental Storefront Registration form to report any property ownership changes or storefront vacancies that occurred between January 1 and June 30, 2022, or the date you sold the property, whichever is earlier. Register on the RPIE portal between July 1 and August 9, 2022.

DOF extended the deadline for co-op/condo boards and managing agents to file prevailing wage affidavits to qualify for the residential co-op/condo tax abatement. The extended deadline is June 30, 2022. Certain properties must submit an affidavit certifying that all building service employees employed or to be employed at the property shall receive the applicable prevailing wage for the duration of such property’s tax abatement.

Property tax reform was absent from the New York State budget. It has now been a quiet six months since the NYC Advisory Commission on Property Tax Reform released its final report recommending the most significant changes to NYC’s property tax system in 40 years.

Contact me or another Rosenberg & Estis attorney to see how we can help you reduce your New York City property taxes.

Benjamin M. Williams Head of Property Tax Department (212) 551-1246 [email protected] |